AI Data Center Boom Poses Challenges for Power Generation

Introduction

The data center industry is undergoing a massive expansion, fueled by the growing demands of artificial intelligence (AI) and autonomous technologies. This growth places an unprecedented strain on existing power grids and generation infrastructure. Addressing these constraints requires significant investments in grid capacity and the adoption of diverse energy sources. Emerging trends highlight a strategic pivot toward natural gas, nuclear energy, and behind-the-meter power solutions to secure reliable electricity for high-density computing facilities.

Trends and Innovations

Data center infrastructure’s rapid scale-up creates significant challenges for global power generation and grid capacity.

Data centers are the foundational infrastructure of the modern digital economy. They process, store, and distribute the vast amounts of information required for everyday technological operations.

The exponential growth of AI workloads fundamentally alters the power requirements of these facilities. Advanced computing processes require significantly more electricity than traditional data storage and routing.

Global Data Center Development

Global data center development represents approximately $5.21 trillion in active projects, according to Industrial Info Resources data as of May 14, 2026. This massive capital expenditure spans multiple continents, reflecting a universal need for expanded computing capacity.

Regional hotspots for this development include the United States, Asia, Europe, and Latin America. Secondary markets also are emerging as traditional hubs, but they face severe power transmission constraints.

Major projects illustrate the scale of this expansion. For example, Google is developing two separate $10 billion projects in Missouri: Project Mica and Kestrel.

AI and Inference

AI is rapidly moving beyond basic machine learning into autonomous workflows and embodied intelligence. This shift creates a need for substantial inference capabilities.

Inference workloads involve applying trained AI models to new data sets to make predictions or decisions. This process is inherently power intensive, demanding constant high-speed computation.

The demand for localized inference capabilities at the network edge further increases power requirements across distributed data center facilities.

Huge CapEx Plans for Data Centers

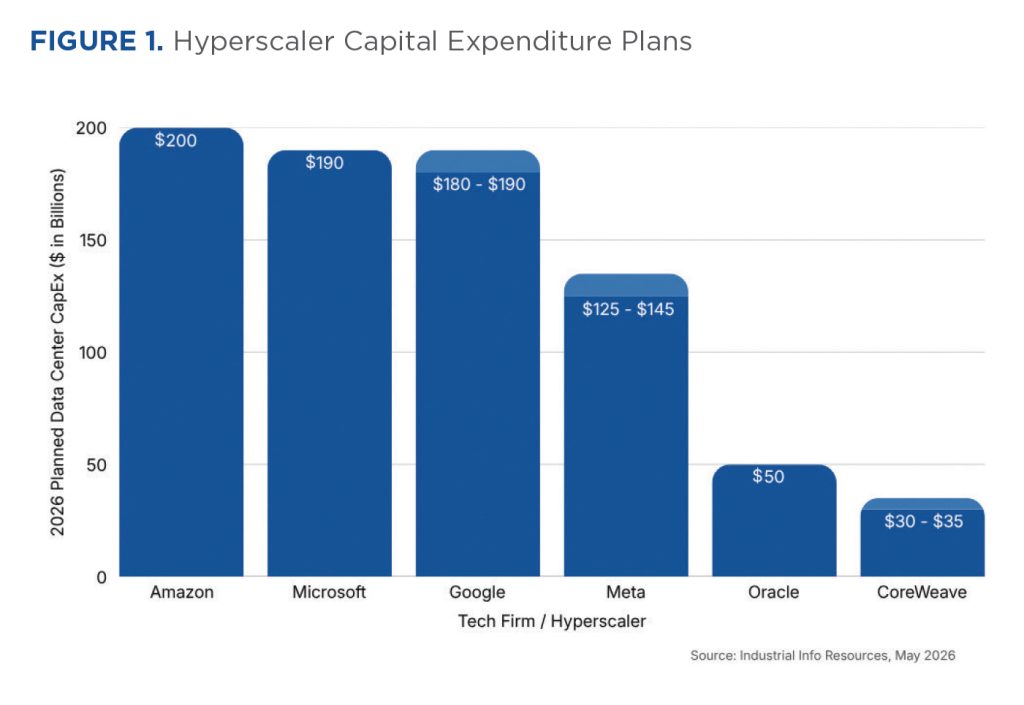

Planned capital outlays to build data centers have been turbocharged by announcements from big tech firms during recent earnings calls with investors, bankers, and analysts. For example, last year, Apple said it would invest $10 to $15 billion annually in U.S. data centers over the coming 4 years. Figure 1 illustrates the CapEx projections for six additional firms.

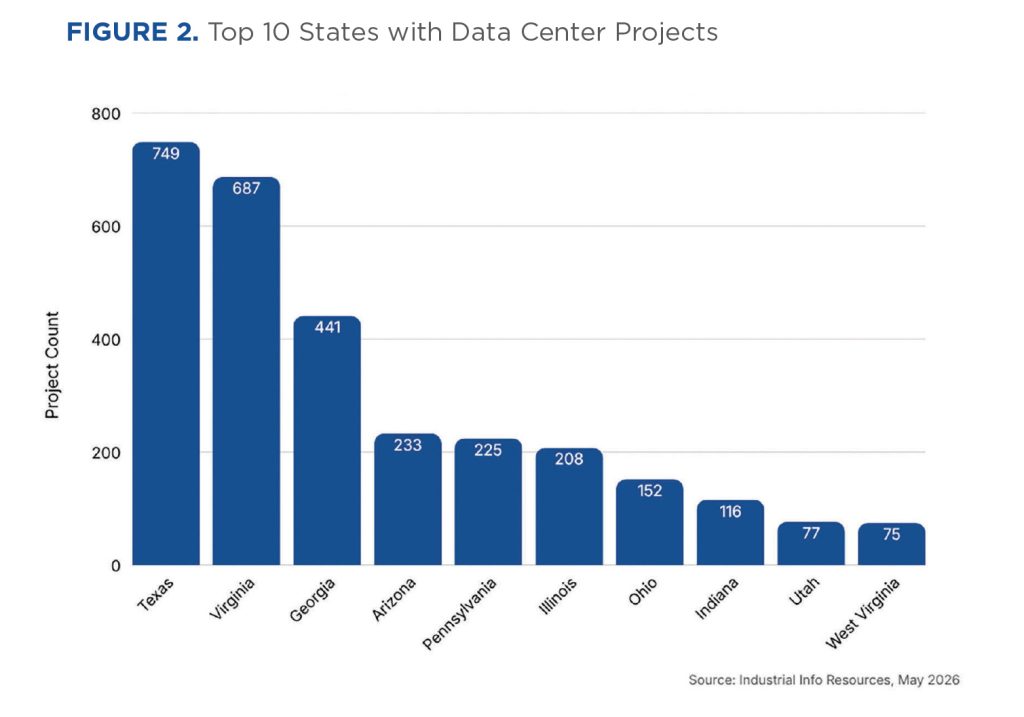

“Industrial Info Resources does not expect all proposed U.S. data centers over the 2026–2030 period to begin construction as planned,” said David Pickering, Industrial Info Resources’ Vice President of Research for the Industrial Manufacturing sector, which includes data centers. “This is an extraordinarily dynamic industry, both in terms of technology advancement and AI aspirations. Projects will drop out. Projects will be delayed, typically due to supply chain bottlenecks. But new projects are sure to be added.” Figure 2 shows the top 10 states in terms of data center projects.

Power Projections

Projections indicate that power consumption by data centers in the United States will triple by 2030. This surge represents an unprecedented increase in industrial electricity demand.

Under current models, data centers will consume approximately 12% of the power on the U.S. electric grid by 2030. This growth path anticipates an additional 90 gigawatts of electric demand solely from computing facilities.

Driven by a concentration of data centers, as well as electric vehicles and building electrification, commercial electricity sales in Virginia alone increased by nearly 30 million megawatt hours (MWh) between 2019 and 2025. This represents much faster growth than in any other state except Texas, according to the U.S. Energy Information Administration.

In Europe, data center electricity consumption is projected to more than double by 2030, as planned data center capacity is constructed. Data centers currently consume about 1.5% of electricity globally, and this is set to grow.

Worldwide use of electricity by data centers is expected to more than double by 2030, to about 950 terawatt-hours, though there are a number of factors that could push that number up or down, according to a report issued in April by the International Energy Agency1.

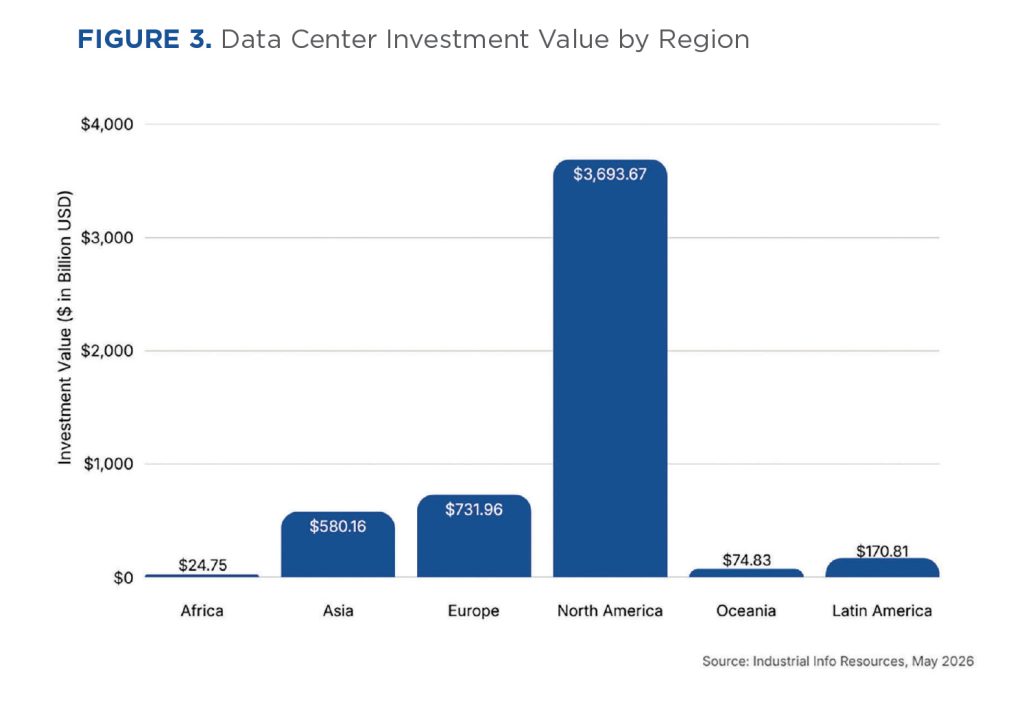

With $3.45 trillion, the U.S. accounts for some 62% of the current $5.21 trillion of active global data center investments, according to the Industrial Info Resources Global Market Intelligence Industrial Manufacturing Project Database. This compares with Europe’s nearly $730 billion and Asia’s $577 billion. See Figure 3 for regional investment data.

Challenges in Power Generation

In just the first quarter of 2026, U.S. businesses invested $44.7 billion in data centers, a 28% gain over the year-earlier quarter, according to data released by the Bureau of Economic Analysis, a branch of the U.S. Department of Commerce.

This growth in data centers places an unprecedented strain on existing power grids and generation infrastructure. The wait times for natural gas-fired power plant turbine deliveries have increased dramatically, stretching up to 7 years in some cases.

Addressing these constraints requires significant investments in grid capacity and the adoption of diverse energy sources. Emerging trends highlight a strategic pivot toward natural gas, nuclear energy, and behind-the-meter power solutions to secure reliable electricity for high-density computing facilities.

Grid Capacity and Transmission Constraints

Securing energized real estate and sufficient grid capacity is the primary bottleneck for new data center projects. Financial capital is readily available, but the physical infrastructure required to deliver power is severely constrained.

Utility companies frequently delay approvals for large-scale projects due to an inability to meet the requested load. In some instances, developers requesting 500 megawatts of power are receiving timelines stretching into 2031 or 2032.

Supply-Chain and Labor Issues

Delays in procuring essential equipment, such as transformers and inverters, continue to hinder project timelines. These supply-chain bottlenecks extend the development cycle for both power plants and data centers.

Labor shortages within the construction and engineering sectors further impact the rapid deployment of new infrastructure. Recruiting skilled workers to build highly specialized computing environments remains a persistent challenge.

Retrofitting Existing Infrastructure

Most existing data centers built since the late 1990s lack the infrastructure to handle modern AI and inference workloads. Older facilities were designed for standard server racks that consume significantly less power.

Newer chipsets and high-density computing racks demand specialized liquid cooling systems. Upgrading existing facilities to support these technologies requires substantial capital investment and temporary operational disruptions.

Environmental and Regulatory Issues

The push for climate-neutral data centers conflicts with the immediate need for dispatchable baseload power. Tech companies face intense scrutiny to maintain aggressive sustainability goals while rapidly expanding their operations.

Shifts in energy policies and the backlog of approvals from independent system operators complicate the integration of renewable energy projects into the broader transmission grid.

Power Generation Innovations and Solutions

The following solutions are being explored to address the growing need for energy.

Behind-the-Meter Power Plants

To bypass extended utility timelines, many developers are turning to behind-the-meter power plants. This involves constructing dedicated power-generation facilities directly on site or next to the data center. Third-party developers are rapidly scaling up services to build these specialized power plants. Specifically, behind-the-meter natural gas plants require extensive acoustic insulation and exhaust system lagging, which are high-margin opportunities for contractors. Notable examples include Elon Musk’s use of natural gas turbines for data centers in Mississippi, and Tallgrass Energy Partners’ proposed 1.8 gigawatt project in Wyoming.

Renewable Energy

Despite regulatory hurdles, the integration of solar, wind, and battery-storage projects continues to grow. Renewable energy remains a critical component for technology companies aiming for carbon neutrality. The primary obstacle remains the backlog of

approvals and grid interconnection processes. Successfully deploying utility-scale renewables requires navigating complex regulatory environments and long wait times.

Liquid Cooling and High-Density Racks

The transition from traditional air cooling to liquid cooling—including chilled water, dielectric, or two-phase immersion—is necessary for high-performance computing and creates a massive demand for closed-cell elastomeric foam and high-performance cellular glass to prevent condensation on chilled lines.

While projections indicate rack densities could eventually reach 600 kilowatts, today’s most immediate infrastructure challenge is the industry-wide transition from traditional 15-kilowatt racks to systems exceeding 100 kilowatts per rack. This transition drastically alters the power and cooling infrastructure design of modern data centers, making conventional air cooling no longer viable. In turn, liquid cooling becomes a mandatory mechanical requirement rather than an optional efficiency upgrade.

Fuel Switching and Repowering

Many power producers are converting existing generation facilities to use lower-carbon fuels like natural gas or hydrogen. This process, known as repowering, leverages existing grid connections to bring new capacity online faster. Companies like Duke Energy and CPS Energy are exploring fuel switching projects to support the increased demand from data centers without relying entirely on grassroot facility construction.

The Role of Manufacturers and Developers

Where and how do manufacturers and developers fit into the picture?

Scaling Production of Power Equipment

Equipment manufacturers are aggressively scaling production to meet the demand for heavy-frame gas turbines and natural gas fuel cells. GE, Siemens, and Mitsubishi are expanding their manufacturing capabilities significantly.

Boom Supersonic is an emerging player, leveraging its proprietary aircraft engine technology to manufacture natural gas turbines for data centers, with Crusoe as its launch customer. Innovations in natural gas boilers and the repurposing of retired aircraft jet engines for ground-based power production highlight the urgency of the equipment supply chain response.

Strategic Shifts by Bitcoin Mining Companies

Cryptocurrency mining companies are pivoting their operations to capitalize on the AI data center boom. These organizations already possess secured power access and active grid connections. Firms like MARA, Riot, and TeraWulf are executing multibillion-dollar strategic shifts to transform their cryptocurrency mining operations into high-performance computing centers for AI.

Nuclear Power Resurgence

The power demands of data centers are driving a significant resurgence in nuclear energy. Tech companies view nuclear power as a vital source of firm, carbon-free baseload electricity. This resurgence includes the planned restarts of dormant facilities like the Palisades plant in Michigan and the Crane Clean Energy Center (formerly Three Mile Island) in Pennsylvania. Additionally, developers are advancing projects focused on small modular reactors to provide localized, scalable nuclear power.

The resurgence of nuclear generation is also expected to renew long-term demand for high- temperature thermal insulation systems used on steam lines, process piping, and power generation equipment. Materials such as calcium silicate and mineral wool, long utilized throughout conventional power generation, are likely to see renewed demand as dormant facilities restart and new small modular reactor projects advance.

Construction began in April on two long-planned nuclear power projects, one in Wyoming and the other in Tennessee. Industrial Info Resources data show developers and nuclear plant operators have scheduled approximately 111 capital projects for the nuclear sector, with an aggregate value of about $211 billion.

A prior attempt to revive new-build nuclear power in the United States ended ignominiously, with more than 40 capital projects valued at roughly $250 billion being cancelled or placed on hold. But this time, the nuclear power industry has two new and powerful allies: data center hyperscalers and U.S. President Donald Trump.

The Outlook

What can we expect in the near future?

Forecast for Power Demand Growth

- The United States has not experienced electric demand growth of this magnitude since the 1970s.

- The convergence of data center expansion and industrial manufacturing growth is reshaping energy forecasts.

- Projections indicate more than 160 gigawatts of total new electric demand across all sectors by the early 2030s. Meeting this demand will require a coordinated effort across all forms of power generation.

Modernizing the Transmission Grid

- Much of the existing transmission grid is over 40 years old and ill-equipped to handle the routing of massive new power loads. Significant investments are necessary to renovate and modernize this critical infrastructure.

- Major utilities like Dominion, Duke Energy, and NextEra are committing tens of billions of dollars to grid modernization. These investments will ensure power can move reliably from generation sources to high-density data hubs.

Balancing Sustainability and Growth

- The industry must balance the urgent need for power with long-term environmental sustainability.

- Achieving climate-neutral data centers will require continued investment in renewable energy and carbon-capture technologies.

- Innovations that improve energy efficiency at the chip level and the facility level will be vital for mitigating the environmental impact of unprecedented computational growth.

Conclusion

The rapid expansion of AI drives an immediate and profound need for expanded data center infrastructure and, by extension, power-generation capacity.

Addressing this challenge requires overcoming grid bottlenecks, scaling equipment manufacturing, and exploring energy sources like natural gas and nuclear power.

Stakeholders across the power-generation and technology sectors must prioritize collaboration and strategic investment.

For the mechanical insulation industry, the AI boom isn’t just about “digital growth.” Rather, it represents a fundamental shift in fluid dynamics and thermal management. Whether it’s insulating the 400°F steam lines of a restarted nuclear reactor or the 45°F chilled water lines feeding a 100kW AI rack, the demand for precision-engineered insulation has never been higher.

Reference