2023 North American Engineering and Construction Outlook—Second Quarter Edition

Summary

Last year FMI altered base case assumptions for our forecasts to include a multiyear recession spanning into 2023. As with historical cycles, impact on the construction industry will be longer-lasting.

Economic factors influencing this forecast include the recent banking challenges impacting expectations on lending standards and ongoing consolidation; shortages of key materials and labor across various industries; ongoing strain on global logistics infrastructure; volatility across real estate; Federal Reserve policy; and continued inflationary pressures. We also considered wartime and economic turmoil in various countries (e.g., Russia, Ukraine, and China) adding to strain and uncertainty on each of these items.

It is important to recognize that FMI anticipates the U.S. economy will fare better than most countries, as reflected by strong demand for labor and the long-term commitment to infrastructure investments. As a result, the engineering and construction industry is expected to play a major role in our economy’s foundational strength over the coming years, offering a combination of both challenges and opportunities.

Key U.S. Takeaways

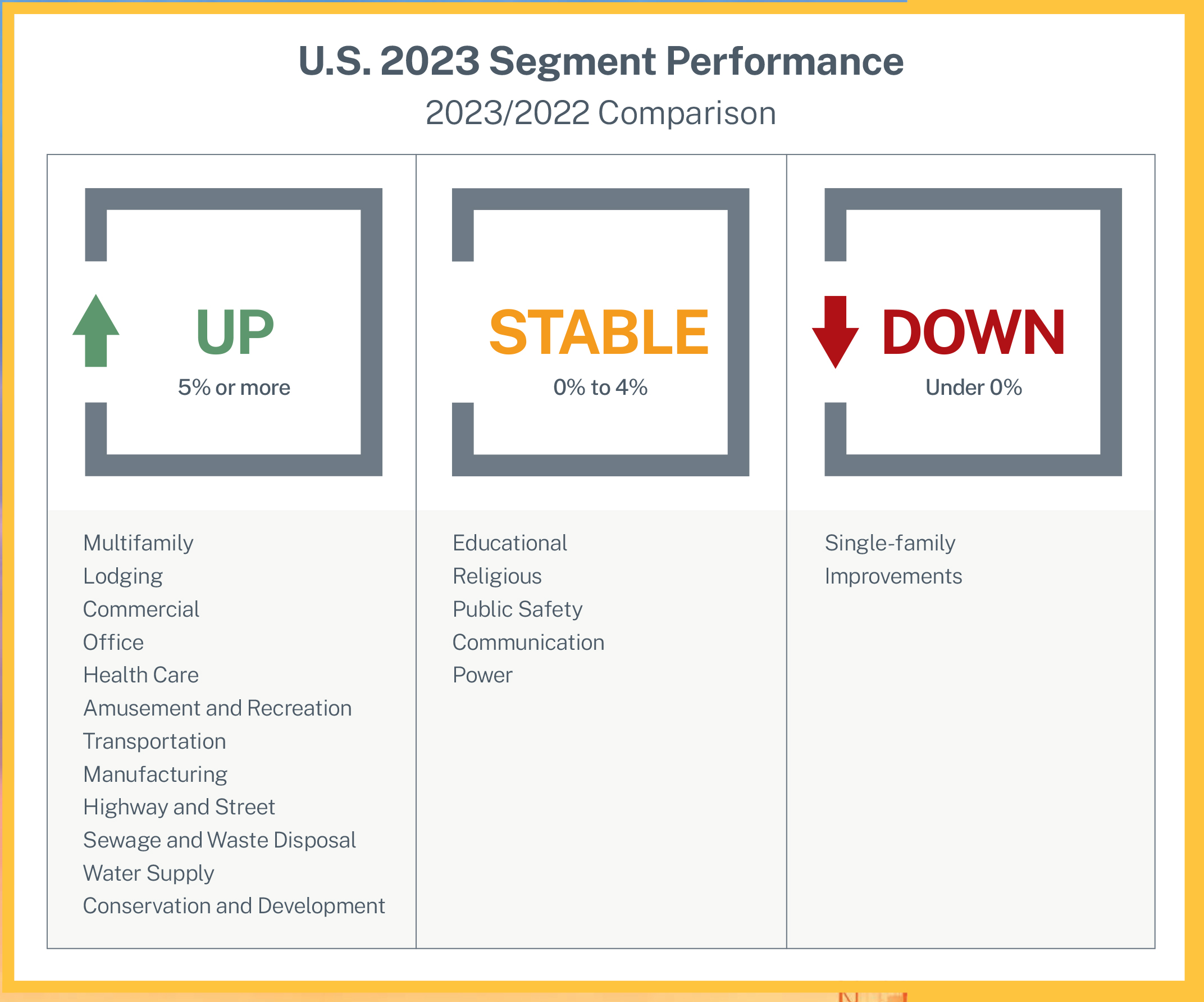

- • Total engineering and construction spending for the U.S. is forecast to end 2023 down 1%, compared to up 11% in 2022.

- Steep declines in single-family residential and residential improvements will lead a contraction in overall industry spending while most nonresidential building and nonbuilding structure segments are expected to experience growth through 2023.

- Strong investment growth is expected across lodging, commercial, transportation, manufacturing, highway and street, water supply, and conservation and development, each with year-over-year growth rates nearing or exceeding 10%. Additionally, above-average investment growth is anticipated across office, health care, amusement and recreation, and sewage and waste disposal.

- Corrections in residential construction spending are anticipated into 2026, due to softening economic conditions tied to rate hikes and a recession. Consistent with historical industry cycles, similar corrections are expected to bleed over into nonresidential segments beginning late 2023 and into 2024.

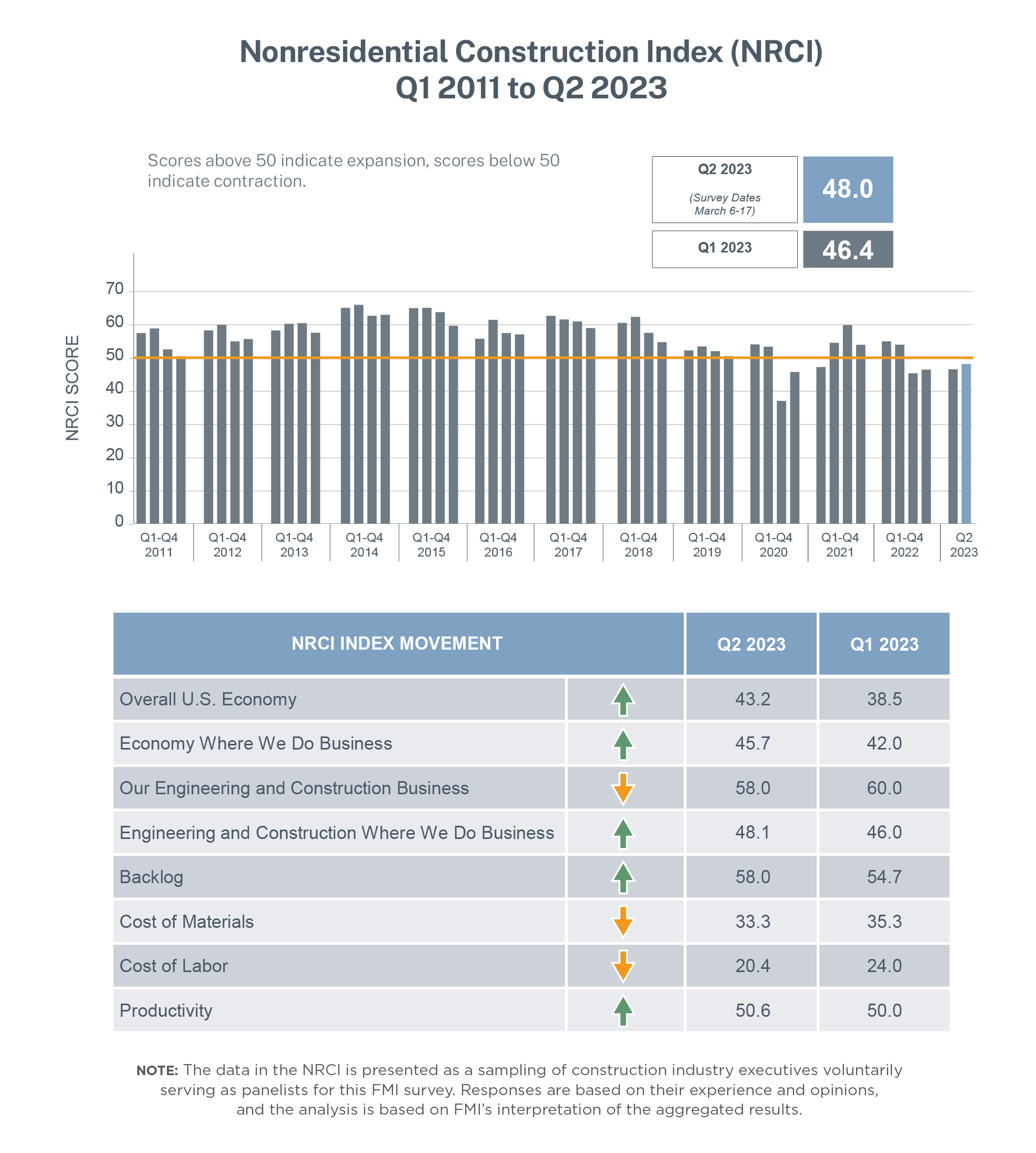

- The latest Nonresidential Construction Index (NRCI) reflects the fourth straight quarter of ongoing challenges, with a reading of 48.0, up slightly from 46.4 in the quarter prior.

Sentiment this quarter was slightly improved based on increased optimism toward the overall U.S. economy and local factors impacting the economy and nonresidential industry where participants are operating their businesses. However, the index remains below the growth threshold of 50 and reflects declining engineering and construction

Conclusion

For details on this forecast, visit www.fmicorp.com. FMI is a leading consulting and investment banking firm dedicated to serving companies working within the built environment. Our professionals are industry insiders who understand your operating environment, challenges, and opportunities. FMI’s sector expertise and broad range of solutions help our clients discover value drivers, build resilient teams, streamline operations, grow with confidence, and sell with optimal results.