Architectural, Engineering, and Construction CEOs: Sentiment Index Reflects Optimism while Design Index Slips

The Construction Industry Round Table (CIRT) is composed of approximately 130 CEOs from the architectural, engineering, and construction firms doing business in the United States. The first quarter 2025 CIRT Sentiment Index increased to 67.9 from 64.1 in the fourth quarter of 2024, reflecting optimism and expectations for the industry not seen since 2021–2022. However, the outlook isn’t as positive among those focused solely on design, with the Design Index falling to 61.8 from 71.1 (see Figure 1).

The last time the Design Index and Sentiment Index diverged this significantly was during the economic turbulence of COVID-19 5 years ago. Since then, the design segment has consistently led the trend—rising in expanding markets and declining in those expected to contract. This current divergence could be a signal of something significant and, at the least, suggests that the lag between front-end design activity and its downstream impact on construction has widened. Notably, the rapid and substantial paradigm shifts introduced by the new administration are already being felt in the planning and design stages, though not yet in the subsequent building phase. Either way, this remains a critical trend to monitor throughout the remainder of 2025.

This quarter, CIRT members report slight declines in sentiment across most economic components, including the overall U.S. economy, regional economies where members operate, and members’ own construction businesses—although optimism is up for the nonresidential sector. Respondents also report stronger backlogs and productivity but anticipate higher labor and material costs in the coming months.

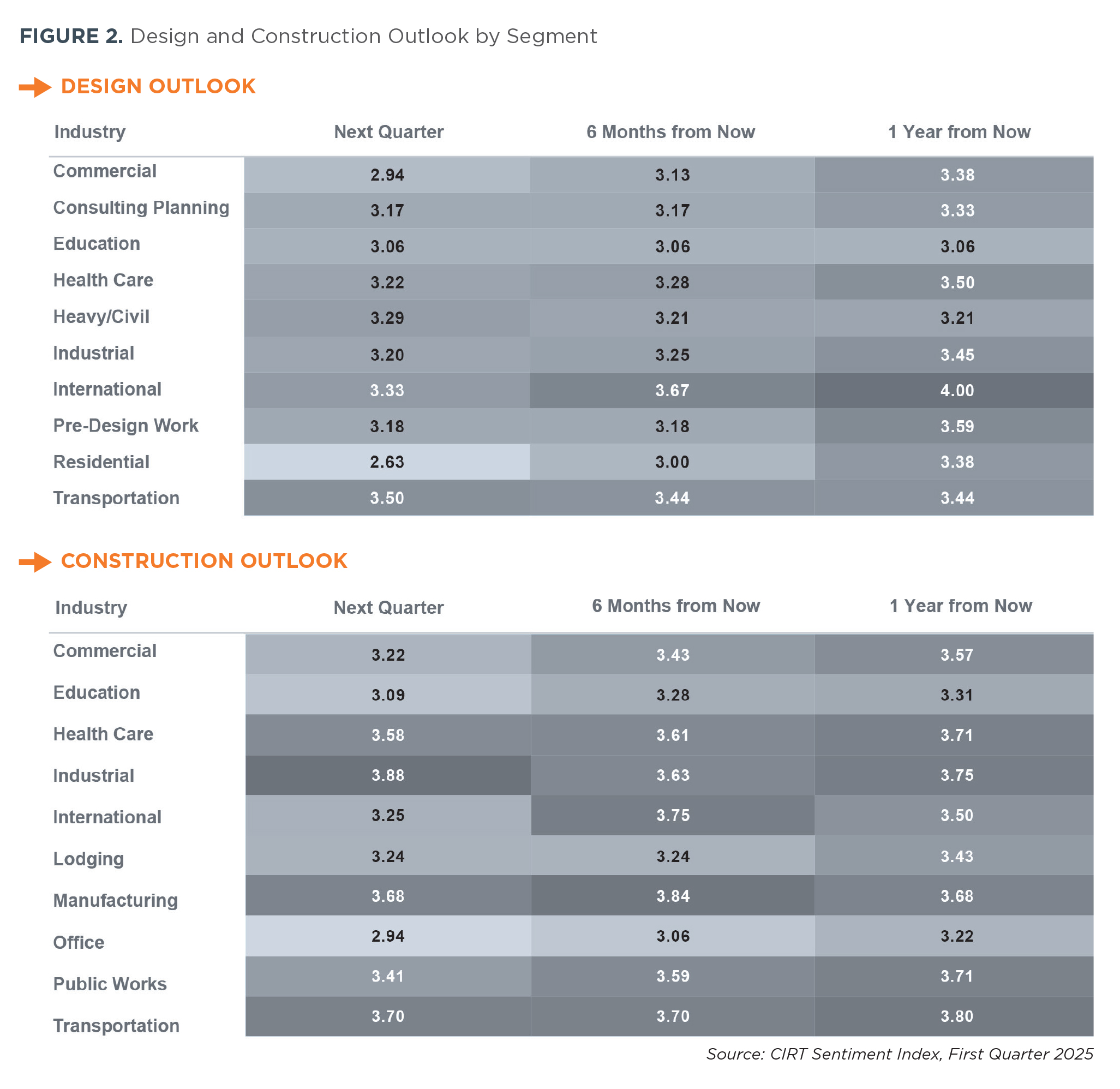

Compared to the previous quarter, design sentiment toward individual segments improved, driven by strengthened expectations in residential work, with continued optimism in health care, education, predesign work, and consulting planning. In contrast, sentiment weakened in heavy civil, transportation, and commercial design. Construction sentiment remains stable overall but varies by segment: commercial, office, lodging, education, and health care sentiment improved, but for manufacturing, public works, industrial, transportation, and international expectations, it declined (see Figure 2).

CIRT members were asked this quarter to respond to current-issue questions focused on their backlogs, capacity and hiring goals, procurement, delivery methods, selection criteria and top challenges expected in 2025.

Backlog levels remain strong, with nearly half of respondents maintaining backlogs of 19 months or longer, though firms must navigate labor constraints to effectively meet demand. Firm capacity has declined since 2024, with more than half of respondents reporting labor shortages relative to backlog needs, leading to mixed hiring outlooks. While labor availability remains the top challenge for 2025, geopolitical instability, including trade, tariffs, and commerce disruptions, has emerged as a growing concern, particularly considering recent political transitions.

Procurement trends highlight inconsistent technology adoption and prolonged decision- making, with major projects often taking longer than 6 months for firms to finalize. Clients continue to prioritize cost and experience in making selection decisions, while quality and innovation remain secondary considerations. Design-bid-build remains the dominant delivery method, although interest in alternative models such as design-build and construction manager at risk is increasing, driven by risk transfer, speed to market, and regulatory considerations.

Among the industries represented by CIRT’s members, segment expectations remain mixed. In the near-term, design expectations are weakened across most sectors except transportation, while long-term optimism is up for international work. Conversely, sentiment has shifted from expansion to contraction for consulting planning, industrial, heavy civil, residential, and predesign work looking to 2026. Within the construction sector, manufacturing, industrial, and transportation show notable strength over the last quarter. Moderate improvements have also emerged in commercial, lodging, health care, international, office. and public works. However, education has weakened and, along with lodging and office, is expected to remain challenged into next year.