Gazing into the Crystal Ball 2008

Construction Market Forecast: Nonresidential Construction Declines in Some Segments in 2008

FMI, management consultants and investment bankers to the building and construction industry, announces the Construction Outlook: First Quarter 2008 is now available. The Construction Outlook, a quarterly construction market forecast developed by FMI’s Research Services Group, notes that FMI’s outlook for construction for 2008 and 2009 has been revised down since the fourth quarter of 2007.

Recently released economic indicators are far bleaker than the previous months. The housing downturn, weakening employment rates, worsening consumer confidence, credit tightening and the threat of inflation are all factors expected to be drags on the economy, the report indicates.

Nonresidential Construction

Nonresidential construction will see declines in 2008 and 2009, except some publicly funded segments.

The nonresidential segments that are the most cyclical, or tied to the economy, will see declines in 2008 and 2009. These segments include office, commercial, religious and amusement and recreation. Lodging is the only exception as there is enough overhang from starts in 2007 that are still under construction in 2008.

Publicly funded nonresidential segments will fare much better, such as health care, educational, public safety and Homeland Security construction.

Health care construction will remain positive partly due to facility upgrades across the country and seismic retrofits in California. Education construction will decline in some areas of the country due to less property taxes and therefore less state revenue. However, many MSAs and school systems in several states have passed education bonds, which will help to stop growth from turning negative. Higher education will experience steady growth driven by an increase in endowments. Public safety construction will grow because of increasing inmate populations (which is rising faster than the general population growth) and an increase in fire and police stations. Homeland Security port and border work and port work to increase port size to be able to accept post-Panamax sized vessels will help to drive transportation construction. Increased airport delays will also increase construction.

Residential

Housing will affect the economy again in 2008. It is not expected to begin recovering until 2009. All segments of the residential sector will remain down, led by single family (-10%), followed multi family (-7%) and then finishing with improvements (-2%).

Manufacturing

The report also comments on manufacturing. FMI believes it will not experience decreases in 2008 and 2009 partly because it is at a low level; its previous high from 1998 will not be surpassed until 2010. Manufacturing will also benefit from the overhang of some huge projects started in 2007. For the first time, several multi-billion dollar projects are under construction at the same time. Basic materials manufacturing will also help to prop up this segment. Increases in cement clinker capacity, refineries and steel manufacturing will contribute to these gains.

“The economic indicators look bleak for construction in the upcoming year, but the outlook is optimistic for a few nonresidential and nonbuilding segments,” said Heather Jones, construction economist for FMI’s Research Services. “The segments that will remain positive in 2008 are either non-cyclical or are being propped up by large starts last year. The slowing economy will cause total nonresidential construction to decline in 2009 as lower starts in 2008 are finally felt.”

Historical information in Construction Outlook is based on building permits and construction put in place data as provided by the U.S. Commerce Department. Forecasts are based on econometric and demographic relationships developed by FMI, on information from specific projects gathered from trade resources and on FMI’s analysis and interpretation of current and expected social and economic conditions.

Heather Jones, a construction economist for FMI’s Research Services, is responsible for design, management and performance of primary and secondary market research projects and related research activities, including economic analysis and modeling, construction market forecasting and database management. For more information about Construction Outlook: First Quarter 2008 or Heather Jones, contact Tom Smith at FMI Corporation at 919-785-9236 or tsmith@fminet.com.

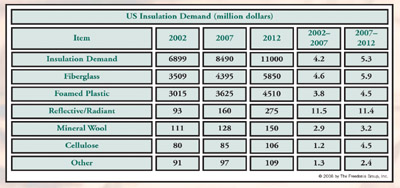

US Insulation Demand to Reach $11 Billion in 2012

Insulation published in March 2008 by the Freedonia Group researches and forecasts the insulation industry.

Demand for insulation materials in the United States is forecast to advance 5.3 percent per annum through 2012 to $11 billion. Consumption will also benefit from greater insulation use on a per structure basis, as well as insulation upgrades for existing buildings, both residential and nonresidential.

Fiberglass insulation will remain the leading insulation material in use, accounting for more than half of demand in dollar and volume terms in 2012. Growth will be driven primarily by the rebound in new home building, the dominant market for fiberglass insulation. Demand will also benefit from more intensive use of fiberglass insulation per new housing unit, sparked by growing concerns about energy efficiency, and by ease of installation and favorable cost factors.

Foamed plastic insulation is the second largest insulation product in use in the US, accounting for nearly 45 percent of demand in value terms in 2007. Advances will derive from growth in nonresidential building construction activity and increasing penetration of residential markets. Other insulation materials, including reflective insulation and radiant barriers, cellulose, mineral wool, perlite, vermiculite, cotton and other materials, all have niche applications. Reflective insulation and radiant barriers will see the fastest growth (albeit from a small base). These insulating materials will find increasing use in metal buildings and other nonresidential structures, as well as in pipe wrap, appliances and duct insulation, as a means of reducing energy costs.

In 2012, residential construction will account for over 45 percent of demand for insulation in value terms and 60 percent in terms of R-1 insulating value. Gains will be most robust in new construction applications, as the industry recovers from a dreadful 2007 trough. Nonresidential construction markets will also provide growth opportunities, although value gains will be about the same as in the 2002-2007 period, and below the overall average.

The South region is the largest geographic market for insulation, accounting for 38 percent of demand in 2007. The South and the West will post the fastest growth in demand as they continue to benefit from growing populations, better than average economic growth and generally healthier construction activity. The Northeast and Midwest regions, by contrast, will both record below average gains.

Insulation (published 03/2008, 298 pages) is available for $4,600 from The Freedonia Group, Inc., 767 Beta Drive, Cleveland, OH 44143-2326. For further details, please contact Corinne Gangloff by phone 440.684.9600, fax 440.646.0484 or e-mail pr@freedoniagroup.com. Information may also be obtained through www.freedoniagroup.com.

Figure 1

Figure 1