NIA Surveys Confirm Market Expectations and Forecast Growth in 2021–2022

The Commercial and Industrial Mechanical Insulation and Laminated Metal Building Insulation Markets Are Impacted by the Pandemic

Every 2 years since 1997, NIA has conducted a survey to gauge the size of the mechanical insulation industry; and since 2013, it has also surveyed the laminated metal building insulation segment. The surveys are sponsored by NIA’s Foundation for Education, Training, and Industry Advancement (“the Foundation”) to provide valuable data regarding market size and growth rates for the U.S. commercial and industrial mechanical and laminated metal building insulation markets.

The mechanical insulation survey goes to NIA’s Associate members, who are manufacturers of insulation products or accessories. The laminated metal building insulation survey goes to the Associate members who manufacture products related to metal building insulation. Both surveys ask members to provide information about their sales volume, and then a third-party company—using survey response information and formulas created by NIA—determines the annual size of the respective U.S. insulation industry segments. The methodology used to calculate the results has been consistent, which provides assurance of the validity of comparing year-over-year results. The results and methodology of each survey are discussed separately below.

The latest surveys were conducted in the first quarter of 2021. Questions covered 2019 and 2020, the year of the pandemic, and gathered forecasts for 2021 and 2022. Anticipating a negative impact created by the pandemic in 2020, the most recent surveys contained a few pandemic-related questions in an effort to quantify its impact.

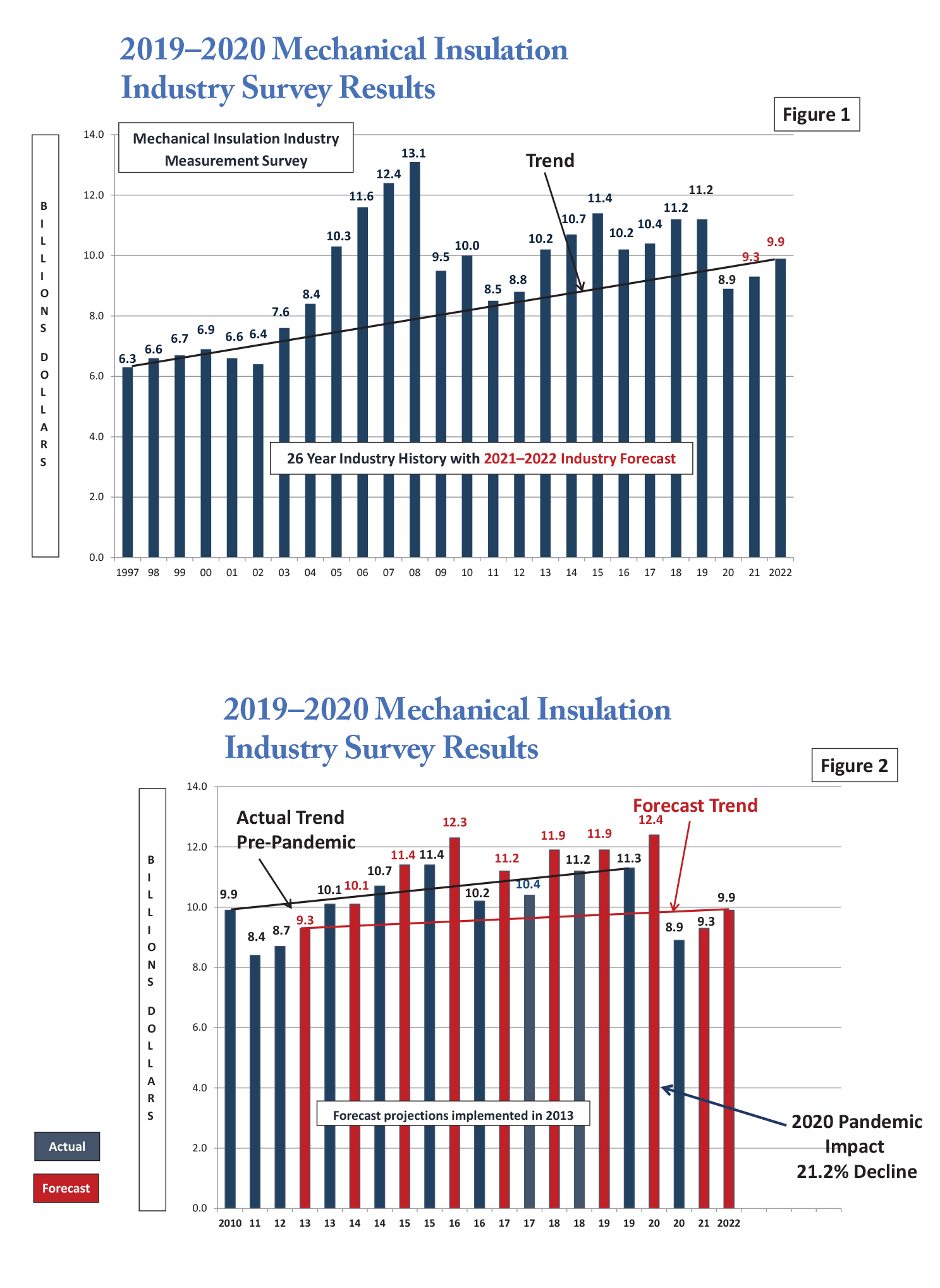

Mechanical Insulation Industry Survey

This survey indicated the overall mechanical insulation industry market grew by .8% in 2019 over 2018, and 2020 saw a 21.2% decline. Growth in 2021 and 2022 is forecast at 4.0% and 6.4%, respectively. The 2022 U.S. mechanical insulation industry is forecast to return to a $10+/- billion level in 2022.

The survey results indicated the material portion had increased by 4.1%, while the labor portion increased .7%. The ratio of labor to material resulted in the .8% overall increase reported.

As we have seen with past surveys, industry growth is not uniform across market segments, the country, by region, by state, or even within states. Figure 1 exhibits the industry growth trend over the last 24 years (1997–2020), inclusive of the forecasts for 2021 and 2022.

While the survey process does not provide a breakdown between what is generally referred to as the commercial and industrial market segments, respondents did indicate on average 55.4% of their insulation materials were utilized in the commercial market, 40.9% in the industrial market, and 3.7% in other markets.

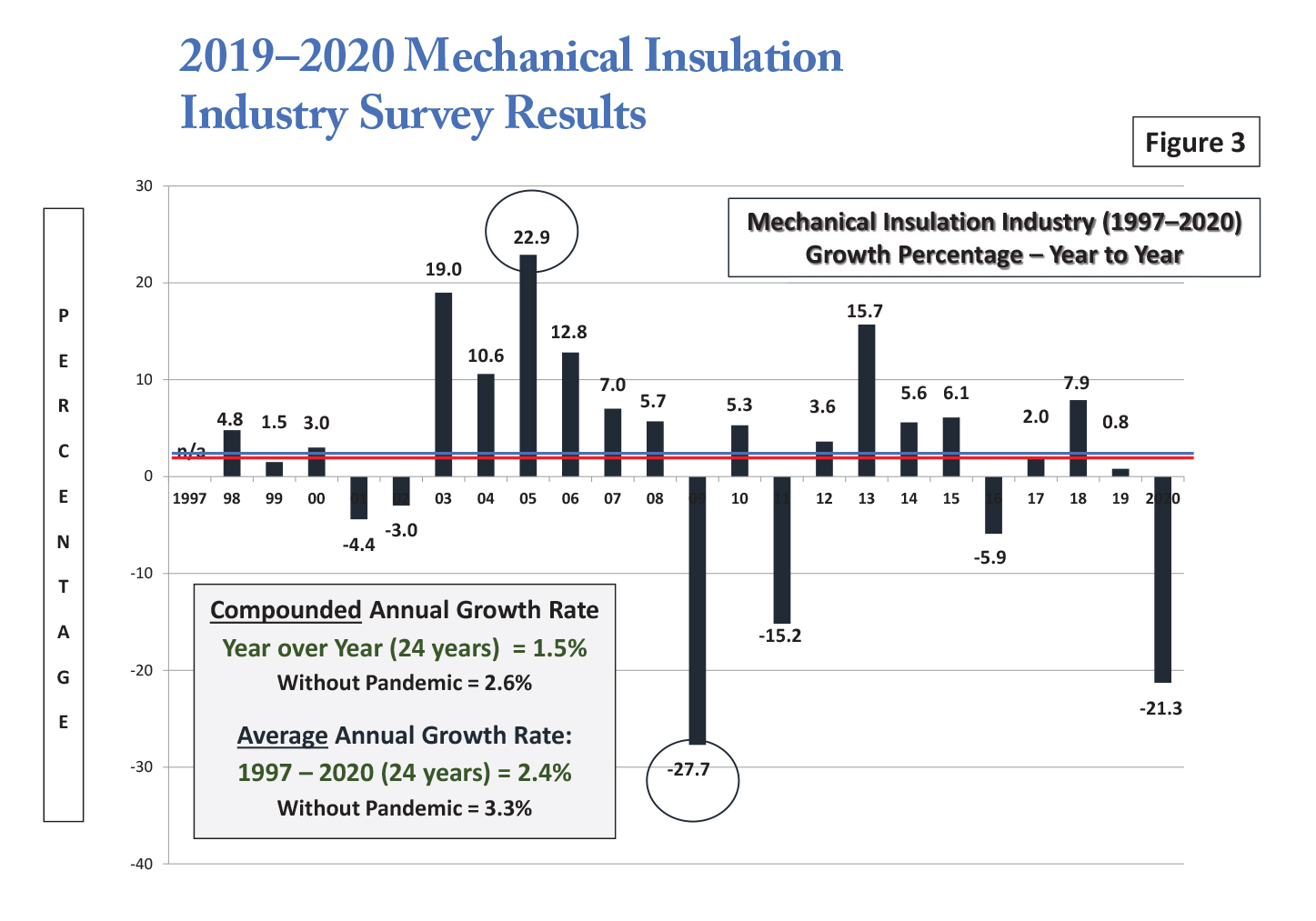

We began including annual forecasts in the 2013 survey. Figure 2 provides a graphic comparison of actual versus forecast growth. Over that 8-year span, on average, actual results have been 96.5% of forecast—even with the pandemic’s impact in 2020. The range of actual-to-forecast results started in 2013 with actual growth exceeding the forecast by 8.6%, compared to a difference between actual and forecast of 28.2%—when actual figures failed to reach the forecast— in 2020, which no one could have predicted.

In the recent survey, 31% of respondents indicated that more than 50% of the decline was pandemic related, 13% indicated 26–50% was related to the pandemic, and 56% indicated less than 25% was pandemic related. This seems to indicate that while a large percentage of the decline was pandemic related, potentially other factors were also impactful.

Consistent with prior years, in an effort to gain a more complete picture, NIA conducted an informal survey regarding the ratio of labor to material among contractors, and sales margins among distributors and contractors.

Beginning in 2017, contractors were reporting a significant change in the labor-to-material ratio. The ratio consists of blended numbers across both commercial and industrial industry segments, and across all types of projects (new construction and maintenance) and contracts. The ratio changed again in 2019 and 2020, from 70% labor/30% material in 2018 to 69%/31% in the recent survey.

The ratio of labor to material varies between commercial and industrial projects or applications. While that ratio in each market segment was not obtained, is it estimated that the greater impact would have been in the industrial segment. The survey calculations are based on an estimated blended ratio. With the methodology used in survey calculations, a

change in the ratio can have a pronounced effect on the survey results. The change in labor-to-material ratio is believed to be driven by a combination of the use of higher cost insulation systems; a larger number of projects utilizing multiple layer/complex insulation systems specifically for cryogenic-type applications; continued growth related to the use of flexible, removable, reusable insulation covers; the growth of fabricated pipe insulation from board products; and similar types of causes.

The survey indicated that, on a national basis, there was gross margin improvement in both the distribution and contractor channels, including in 2020. Many items impact gross margin, and the basis of that improvement will obviously vary by company. However, survey results indicated two items that may have impacted the margin improvement in 2020: the delay or cancellation of larger projects, which historically carry lower margins; and the smaller craft workforce that continued to work was more productive that the previous, larger workforce. While revenue may have been down, margin improvement helped offset a portion of the reduction of gross profit dollars. Of note, we cannot comment on gross margin at the manufacturer level because the survey looked exclusively at manufacturer sales volume.

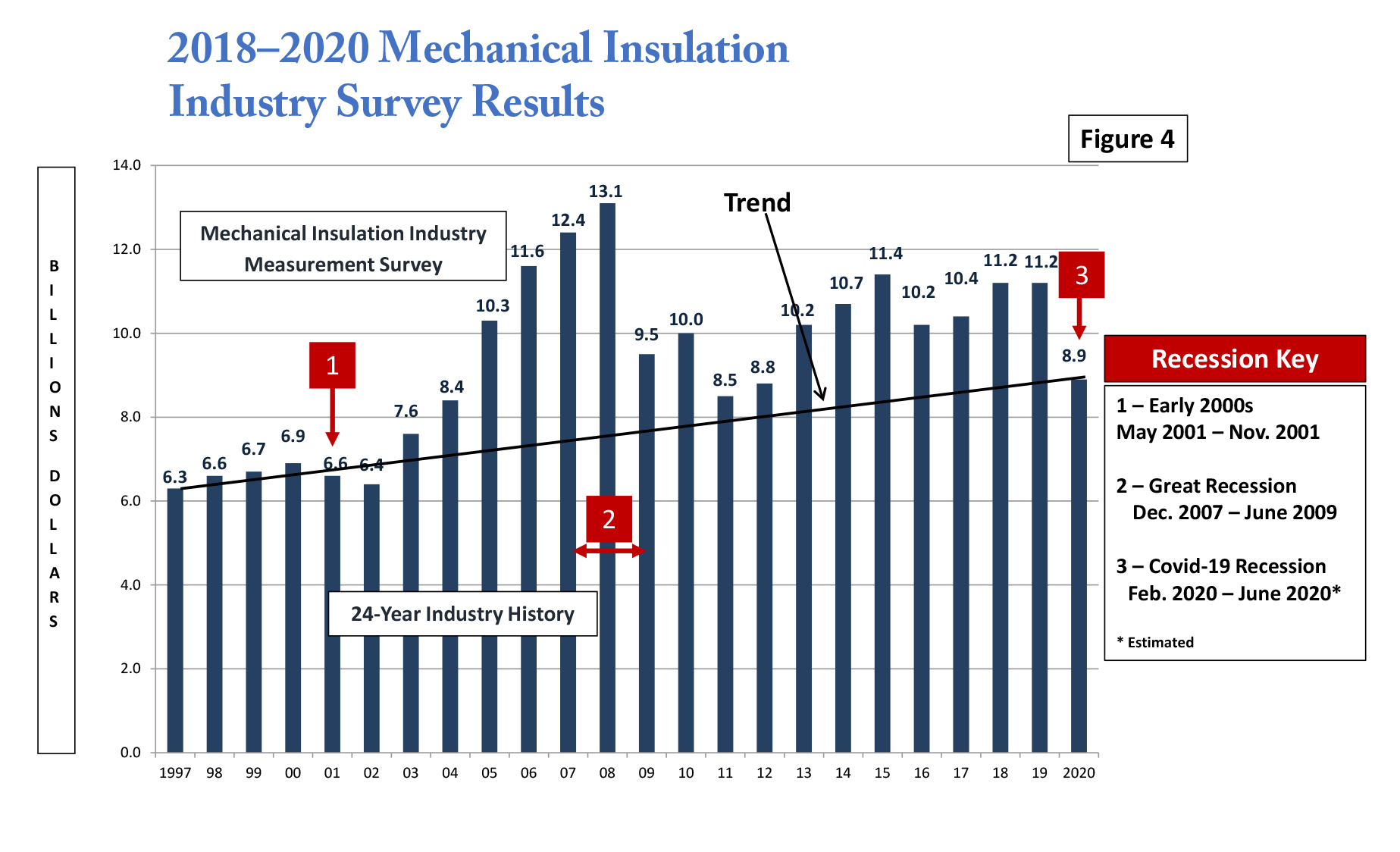

Figure 3 illustrates the industry growth percentage year to year. 2005 marked a high, with a 22.9% annual growth rate, and 2009 marked a decline of 27.7%. While the decline in 2020 was significant, it was not the worst decline the industry has experienced in the last 24 years.

Annual fluctuations are to be expected and are caused mainly by changes in the overall economy. When analyzing industry data in comparison to the economy at large, you need to take into consideration that, due to construction cycles, the mechanical insulation industry typically trails trends for the overall economy between 9 and 15 months.

The compounded annual growth rate, which refers to industry growth over the entire period, is 1.5%, while the average annual growth rate over the period is 2.4%. If 2020 had resulted in zero growth, those numbers would be 2.6% and 3.3%, respectively. For 18 of the last 24 years, the industry has experienced growth. Future surveys will unfortunately need to consider the impact of the 2020 pandemic on historical growth rates.

The recent survey indicates an expected average industry growth of 4.0% in 2021 and 6.4% in 2022. The 2021 increase is expected to occur primarily in the third and fourth quarters.

The range of growth forecast among insulation manufacturer respondents was -8% to +8% for 2021, and +5% to +13% in 2022. Both years, the increase was basically split between unit and dollar growth, with unit growth slightly higher in 2022.

The survey’s confirmation of the pandemic’s impact on the mechanical insulation industry in 2020, potentially carrying over into the first half of 2021, is in line with what economists have said about the United States enduring a short-term COVID-19 recession in 2020. After analyzing the survey results, we decided to look back at prior recessions (after 1997) to see how the duration of those recessions aligned with the annual growth, or decline, in the mechanical insulation industry.

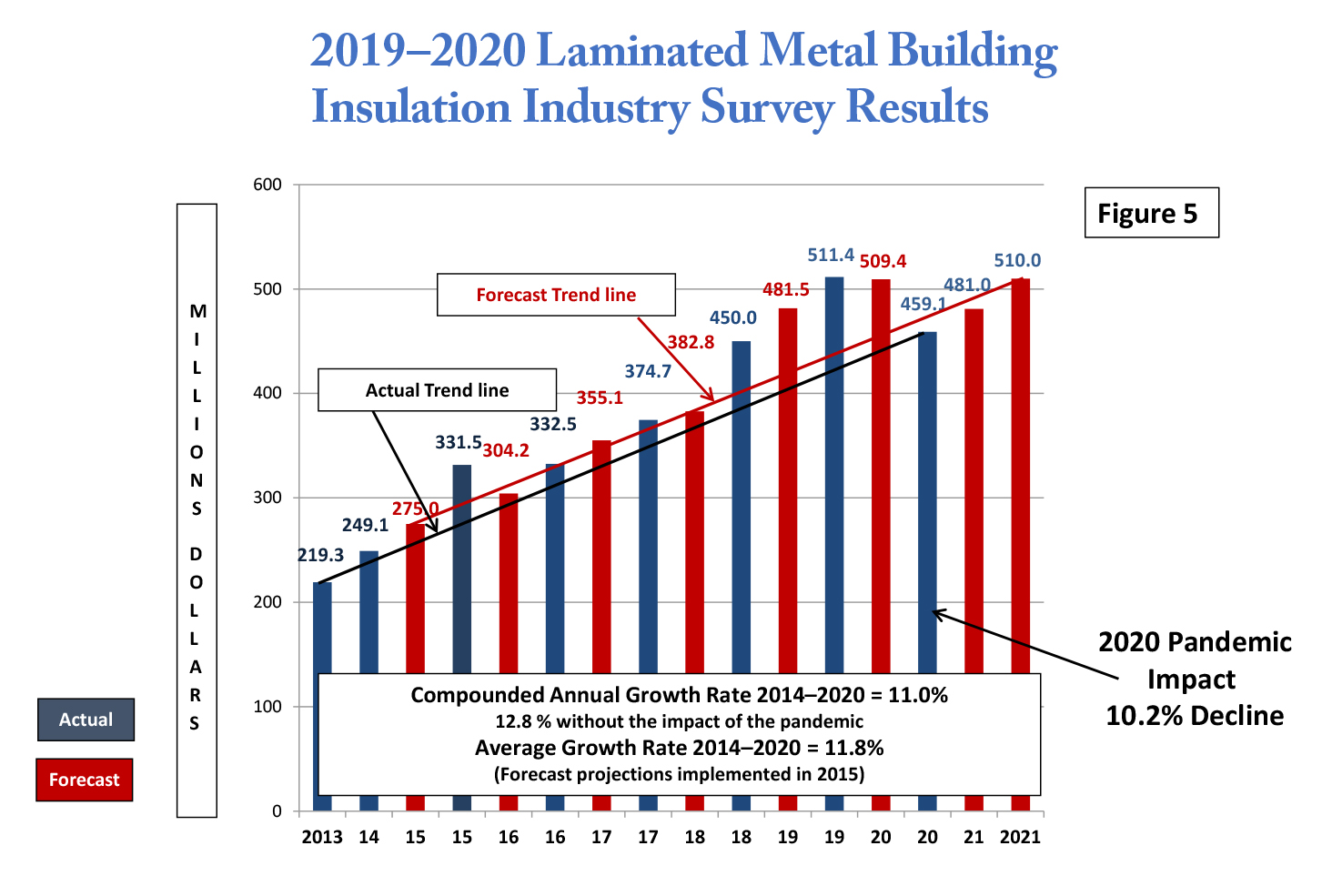

As defined by Lexico.com, a recession is “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.” In the 24 years the survey has been conducted, it is generally recognized that recessions occurred in 2001, 2007–2009, and again in 2020. Figure 4 illustrates those periods in comparison to survey results.

Due to the nature of commercial and industrial construction projects, the mechanical insulation industry typically is one of the last segments to feel the impact of a recession, and one of the last to experience the benefits of recovery. You can see that in Figure 4. While the 2001 recession was short lived, the industry experienced a decline beginning in 2001, continuing through 2002, with a slow recovery starting in 2003. The Great Recession began in late 2007, yet the industry had its biggest year ever in 2008, with a substantial decline in 2009 that lingered through 2012 before sustained recovery began. 2013 through 2019 experienced more normal fluctuations, trending in an upward direction. Then, the COVID-19 recession occurred. The major difference in this recession is that there was no trailing effect. The mechanical insulation industry felt the impact immediately, and the survey results indicate the recovery will be slow, mainly felt in the second half of 2021. In short, the industry is experiencing a different type of recession, but a recession nevertheless.

Methodology and Assumptions

Analysis of any survey’s results is subject to individual interpretation. Following is information about the methodology used and a few assumptions applied in conjunction with tabulation of survey data.

- • The survey is based on dollars, not units, and a consistent approach has been utilized over the 24 years data has been collected (1997–2020). However, the survey does not allow for any analysis as to whether the increases or decreases were led by unit or dollar growth. Based on the survey methodology, the results should represent a conservative number.

- The survey does not include data related to metal building insulation; heating, ventilating, and air-conditioning (HVAC) duct liner; original equipment manufacturer (OEM) products; building/envelope insulation; residential insulation; refractory products; other specialty insulations; or insulation products or technologies not currently within NIA’s scope of mechanical insulation products.

The potential impact of imported products coming from outside North America was believed to be minimal and so was not included in past surveys, nor are they included in the most recent survey. That said, all indications are that the degree of imported products has increased to a point where they should be included in future surveys.

The survey excludes major project scaffolding and similar types of project requirements. - NIA conducted research to determine margins and labor and material ratios. Variations in those results could affect the total insulation market estimate.

- Insulation products include any/all accessory products when sold as an integral part of the manufacturer’s products (e.g., all-service jacket or other facing on blanket, board, or pipe covering).

- The survey is intended to show a “national” picture for the respective calendar year.

Based upon observations, there are significant geographical and product variances in the survey results. This is not inconsistent with any survey of such a broad nature. - The continued growth of flexible, removable, reusable insulation covers, fabricated pipe insulation foam board products, accessory products in insulation systems, insulation system changes to mitigate corrosion under insulation, increased use of prefabricated fitting materials, and a host of other industry trends—combined with consolidation at the manufacturer level—will necessitate review and potential methodology modifications for the 2022 survey. These developments may negatively affect survey results in terms of under-reporting total industry size. While the degree of that impact cannot be determined at this time, it could be in the range of $50+ million dollars.

- The 2021 and 2022 forecasts appear conservative compared to some economists’ projections. However, one must remember that the mechanical insulation industry normally trails construction start projections.

- The forecast does not break out growth expectations between the commercial or industrial market segments, or between new construction, retrofits, and/or maintenance applications. Historically, a forecast of this nature includes a blend of these applications, with new construction being the largest percentage.

- Unfortunately, the survey methodology does not allow for interpretation between the commercial and industrial market segments, or between type of applications, contracts, or product types.

- The Foundation always requests that survey participants share detailed information about their participation in the insulation industry. However, many are only willing to share general information, rather than detailed segment or product line information. In addition, many products are fabricated into different shapes and shipped to various locations for use in multiple industry segments, which makes reporting or forecasting by industry segment or geographic region difficult.

Looking Forward

The mechanical insulation market is once again on the rebound from an unplanned event: the pandemic. Survey results indicate that the industry continues to exhibit compounded growth over an extended period. Some market segments may fluctuate year over year, and occasionally the overall market may experience a decline. As unpredictable and vulnerable to outside influences as the commercial and industrial construction industry seems to be, the mechanical insulation industry continues to stand the test of time, and the future looks promising to survey respondents. The pandemic may have reshaped our industry and our companies in many respects, but the mechanical insulation industry is viewed as resilient and strong.

Laminated Metal Building Insulation Industry Survey

Before 2013, the laminated metal building insulation segment was excluded from NIA’s mechanical insulation surveys because the methodology utilized for mechanical insulation was not applicable for this segment. With the help of several metal building laminators, however, a separate approach and methodology was developed to address the industry segment.

For the purposes of this survey, laminated metal building insulation products are defined as all fiber glass insulation products and jacketing products sold by manufacturers for use in developing (fabricating/laminating) laminated metal building insulation systems. Based on NIA research, the following were added to develop the final survey results: lamination accessory materials (adhesives, packaging, etc.), laminating labor, laminator margin (believed to have remained steady during the period), and delivery costs. The intent was for this survey to represent only laminated metal building insulation, but the methodology employed may have captured some allowance for liner-type products. The survey’s goal is to provide valuable data regarding market size and growth rates for the U.S. laminated metal building insulation market.

Results from this survey indicate that the market continued to grow by double digits in 2019 and declined in 2020, also by double digits. As shown in Figure 5, the U.S. laminated metal building insulation market exceeded $511 million in 2019 (a 13.6% increase over 2018) and declined to $459 million in 2020 (a 10.2% decline from 2019).

The 2020 decline is primarily related to the impact of the pandemic: 100% of survey respondents indicated that 25%+/- of the decline was pandemic related. This indicates, however, that other factors were also impactful.

According to survey responses, the market is forecast to rebound to $481 million in 2021 (a 4.8% increase over 2020), and more than $510 million in 2022 (a 6.0% increase over 2020).

The average annual growth rate since 2013 is 11.8%, and the compounded annual growth rate equals 11.0%. The market has basically doubled in size from 2013–2014 levels.

It is important to note the 2019 survey results exceeded forecast for the fifth consecutive year, with the trend interrupted by the impact of the pandemic in 2020. That trend is nothing less than impressive; and, if it continues, the market would reach $600 million in 2023.

The 2021 forecast is driven primarily by dollar growth versus unit growth, with the reverse holding for 2022. Put the 2 years together and it is basically 50/50. The growth projections for 2021 ranged from 0 to + 9%, and 0 to 15% for 2022. The growth in 2021 is forecast to occur in the later part of the year.

Methodology and Assumptions

As with the mechanical insulation survey, analysis of the laminated metal building insulation industry results is somewhat subject to interpretation. The following is information about the survey methodology, assumptions, and some takeaways developed in conjunction with tabulation of the survey data.

- The survey is based upon dollars, not units, and a consistent approach has been utilized. Based on the survey methodology, the results should represent a conservative number.

- The survey does not include all of the various products utilized in the metal building insulation market, just those outlined above.

- The potential impact of imported products from outside North America has not been included.

- The survey is intended to show a national picture for the respective calendar year. Based on observation, there are significant geographical and product variances in the survey results. This is not inconsistent with any survey of this broad nature.

- Based upon NIA research, it was assessed that while laminator/fabricator margins varied geographically, the overall national average margin has not substantially changed from the previous survey, nor had the ratio between the core insulation and jacketing materials.

- Mechanical insulation and building insulation, including all accessory products, are excluded from this survey.

- The 2021–2022 forecasts seem to be reasonably in line with the overall commercial construction market forecast. The forecast does not break out growth expectations between new construction, retrofits, or maintenance applications. Historically, a forecast of this nature includes a blend of each, with new construction being the largest percentage.

Looking Forward

With the exception of 2020 and the impact of the pandemic, the laminated metal building insulation market continues to sustain annual growth without regard to the fluctuations in the economy. The market has basically doubled in size from 2013 (8 years) and, if the trend of surpassing forecasts continues, it can be extrapolated that the market potentially could triple in size in 11 to 12 years.

Conclusion

Based on responses from the NIA’s recent survey, after a merciless year in 2020—marked by a global pandemic, economic calamity, and uncertainty—the mechanical insulation and laminated metal building insulation industries have endured. As 2021 has been earmarked as the year of healing, even with uncertainty as to how quickly the economy will recover, both industry segments are strong and optimistic. If history is any indication, both segments will rebound with renewed enthusiasm and commitment.

The pandemic may have changed the way people live, work, travel, shop, and interact; but it has not changed the importance and value of insulation, or the commitment and resolve of the people who work in the insulation industry.