Key Global Trends Show Rising Worldwide Demand for Insulation Products

Report identifies opportunities for the insulation industry as demand for energy efficiency, new construction, upgraded equipment, and retrofit applications continue to grow around the world

According to the latest Freedonia Group Global Insulation industry report, looking back to 2021 and ahead to 2026, global demand for insulation is forecast to rise 1.5% per year to $59.2 billion in 2026, with healthy increases in volume demand offset by falling prices. Prices for insulation products spiked in 2021 and 2022 due to supply chain issues and high raw material costs. Prices are expected to moderate significantly through the rest of the forecast period, restraining market value growth. Figure 1 highlights key global trends.

Volume demand is expected to grow 2.7% annually to 29.6 million metric tons in 2026, driven by a number of factors, including:

- Growing manufacturing activity; post-pandemic employees returning to offices on at least a part-time basis; and rising income levels spurring gains in the construction of factories, offices, retail buildings, and other nonresidential structures.

- Efforts in the European Union, the United Kingdom, and the United States to improve the energy efficiency of buildings.

- Rising production of HVAC equipment, industrial equipment, and appliances—particularly refrigerators and freezers.

Regarding the residential building outlook, although continued weakness in housing construction in China and a decline in single-family housing starts in the United States will restrain growth in the residential market, absolute gains will be sizable, supported by trends in both new and retrofit applications. For example:

- New housing construction will be robust in areas with rapidly increasing populations, such as the Africa/Mideast region and parts of the Asia/Pacific region—for example, India, Pakistan, and Malaysia. As living standards improve in these areas, higher quality homes (which are often insulated) will be built.

- Retrofit applications will benefit from a major push among the European Union and the United Kingdom to improve the energy efficiency of homes, as most of Europe aims to reduce energy consumption as the region begins to phase out imports of oil and natural gas from Russia.

About the Freedonia Group’s Global Insulation Industry Report

Global Insulation analyzes the global insulation industry, including both thermal and acoustic products. Visit the product page at http://tinyurl.com/5n8e9v4n to download a sample and see a video summary.

Demand in value terms is shown at the manufacturers’ level and excludes distributor and retailer markups. Insulation materials included in this report include the following.

- Foamed plastic:

• Expanded polystyrene, including graphite polystyrene;

• Polyurethane and polyisocyanurate (e.g., rigid board and spray);

• Extruded polystyrene; and

• Other foamed plastics (e.g., elastomeric, phenolic, polyolefin, and melamine). - Fiber glass (including batts, blankets, loose fill, roof deck, board, and pipe and duct wrap).

- Mineral wool (including batts, blankets, board, and loose fill).

- Other materials (e.g., aerogels, cellulose, reflective insulation, radiant barriers, perlite, vermiculite, and all other insulation materials).

Impact of COVID-19 on the Global Insulation Industry

In general, the COVID-19 pandemic did not result in declines in global insulation demand in 2020, although many countries experienced quarantines and temporary shutdowns of some industries due to government mandates to reduce the spread of the virus. However, growth was minimal in volume terms, as new housing activity or nonresidential construction declined in many major markets.

In 2021, the global insulation market accelerated from 2020, as businesses eased COVID-19 restrictions and new construction activity continued to rise, following the steep drops in the first half of 2020.

A strong increase in appliance insulation demand occurred in 2021, due primarily to not only the fulfillment of previously unavailable appliances but also the elevated levels of home improvement activity in the United States as people spent more time in their home. Consumer demand for new refrigerators, dishwashers, and ovens boosted demand for insulation in appliance applications in 2021.

Another accelerant for the residential market is the solid growth experienced as a result of housing construction recovery in many countries.

Demand for insulation in the transportation market rebounded strongly in 2021, in line with global automotive and aerospace production, as both road and air travel increased substantially from the year before as travel restrictions eased and businesses began to revert to in-office rather than remote work.

Looking at supply chain impacts, in both 2021 and 2022, COVID-19-related supply chain issues and subsequent inflation had a significant impact on the global insulation market. As a result, prices for foamed plastic, mineral wool, and fiber glass insulation increased both years. In addition, there were shortages of both fiber glass and foamed plastic insulation throughout 2021, which caused delays to building projects and further drove up prices as materials became scarce. These price spikes caused insulation market value to grow at an exceedingly rapid rate, with an acceleration in 2022, despite a deceleration in volume demand that same year.

North American Demand

Demand for insulation in North America totaled $13.7 billion in 2021, representing 25% of the global market.

Per capita consumption of insulation in Canada and the United States is among the highest in the world; while in Mexico, intensity of insulation use relative to population size is low by global standards due to the country’s warm climate and less-developed economy.

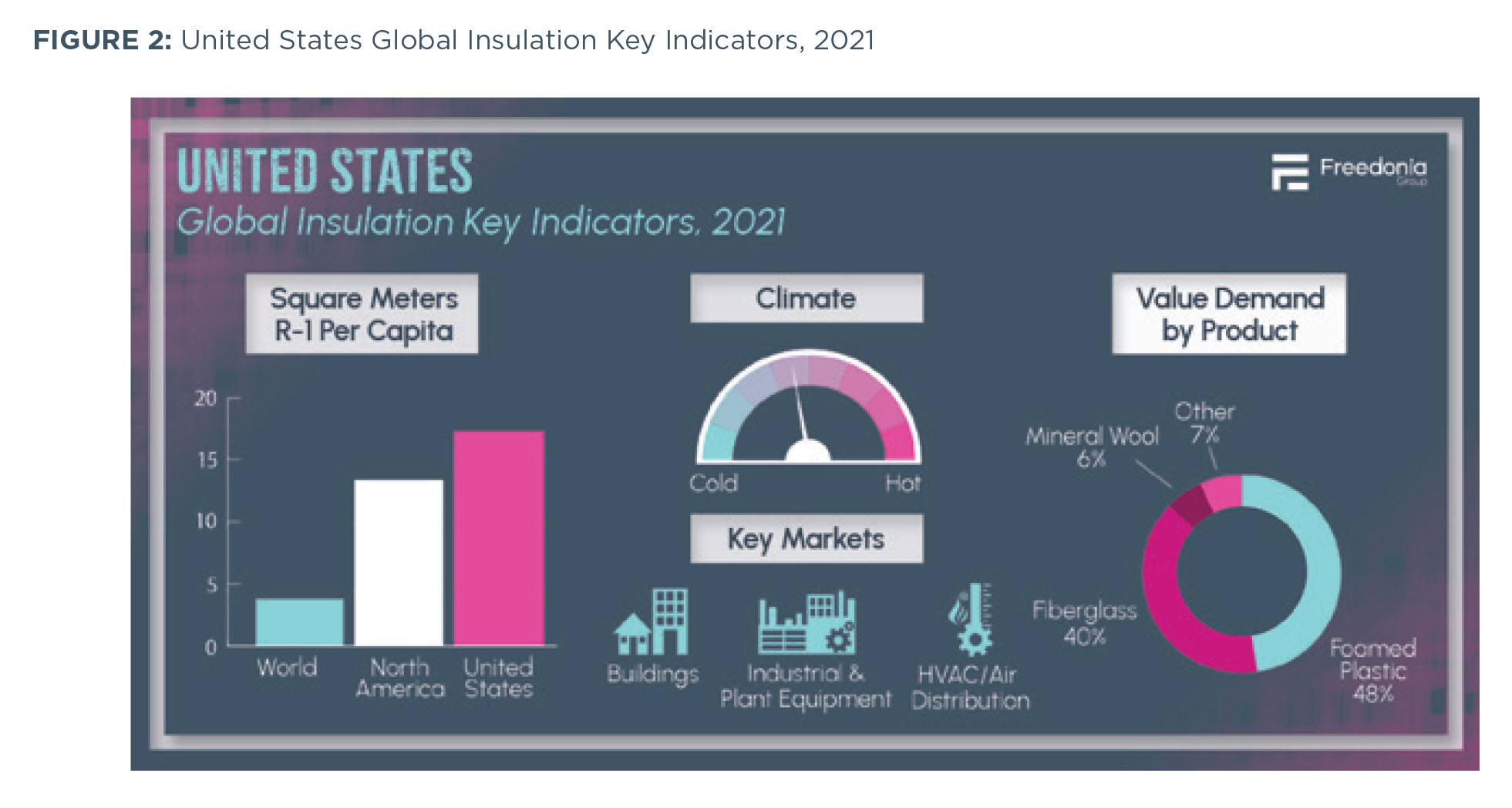

- In value terms, the United States is the largest insulation market in the world.

- Canada is the region’s second-largest market, with demand supported by its harsh, cold climate; high standards of living; large housing unit sizes; and advanced manufacturing base.

United States

In value terms, the United States is by far the largest insulation market in North America, accounting for 86% of regional demand in 2021, and the largest single market in world. (See Figure 2.) The size of the U.S. insulation market is supported by:

- Large average housing sizes and single-family residences accounting for a significant share of the total housing stock;

- Large, highly advanced, and robust manufacturing sector;

- High standards of living, resulting in significant improvement and repair activity in the residential market; and

- Stringent energy-efficiency policies, with rising adoption of modern International Energy Conservation Code building codes.

U.S. demand for insulation is forecast to decline slightly, in value terms, through 2026, as prices moderate from unusually high levels in 2021 and 2022.

Fiber glass is projected to remain the leading insulation material in the United States, in volume terms, due to:

- High consumer familiarity with fiber glass insulation products,

- Its cost and widespread availability,

- A large do-it-yourself attic re-insulation market.

Foamed plastic insulation is the second most popular material by weight and is used extensively in the nonresidential building market, due to ease of installation in steel-frame building construction.

Demand for foamed plastic insulation in the residential market is expected to rise, due to new building codes that call for dwellings to be more tightly sealed to prevent air leakage.

Mineral wool has accounted for a smaller share of insulation demand in the United States, due to a lack of product familiarity and a relatively small production base compared to Western and Eastern Europe, where the material is commonly used.

However, mineral wool will increase its share of the market, in volume terms, due to the

following factors.

- More stringent fire safety codes, which mineral wool insulation is able to accommodate, given its high R-values.

- Cost effectiveness relative to more widely used materials.

- Rising interest in adding acoustical insulation to interior walls in areas of the home such as bedrooms and home theaters.

- Rising construction of hospitals, high-rise buildings, and educational facilities, as flame retardance is an especially high priority in these structures.

- Increasing production of industrial and HVAC equipment, as mineral wool is commonly used in these markets.

India, China, and Indonesia Provide Significant Growth Opportunities

India, China, and Indonesia are projected to be among the fastest-growing insulation markets globally, in volume terms, through 2026 due to several factors.

- Gains in China will be driven by healthy growth in manufacturing activity, most notably for HVAC equipment (as air conditioning increasingly penetrates developing countries) and appliances (as demand increases for quieter and more energy-efficient products).

- Market advances in both India and Indonesia will be driven by solid growth in building construction, particularly in the nonresidential market, as both countries continue to substantially increase their manufacturing bases, resulting in a larger stock of commercial buildings requiring insulation.

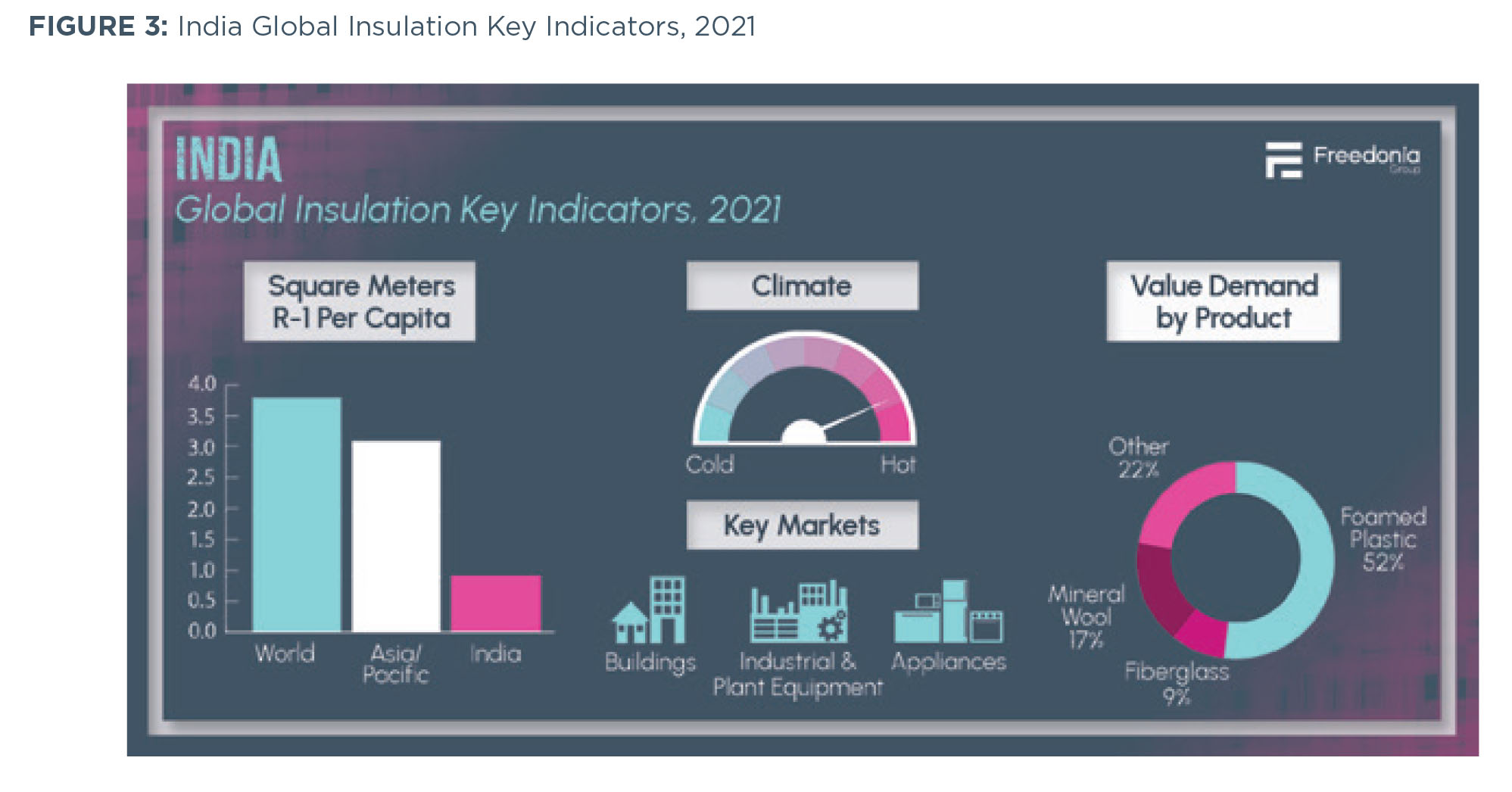

India

In 2021, demand for insulation in India was $1.3 billion, accounting for 7% of regional demand. Figure 3 depicts four key indicators. The size of the domestic insulation market is supported by:

- The world’s second-largest population and housing stock,

- A large nonresidential building construction stock, and

- A sizable appliance manufacturing industry.

However, the market has historically been restricted by:

- Low-quality building construction methods featuring limited insulation installation,

- Limited industrial and high-end transportation equipment production capabilities, and

- Low standards of living.

Demand for insulation in India is expected to rise 4.3% annually, to $1.6 billion in 2026. Factors include:

- Foamed plastic was the most popular insulation material, in value terms, in India in 2021, benefiting from its widespread use in the country’s large appliance and nonresidential building markets. In volume terms, demand for foamed plastic insulation is primarily met by EPS.

- Mineral wool, which accounts for the largest share of demand in volume terms, will climb at the fastest rate, bolstered by the material’s continued use in the rapidly growing nonresidential, industrial, and OEM markets.

- Growing residential building construction and an increase in retrofitting existing residential buildings will spur demand for fiber glass insulation.

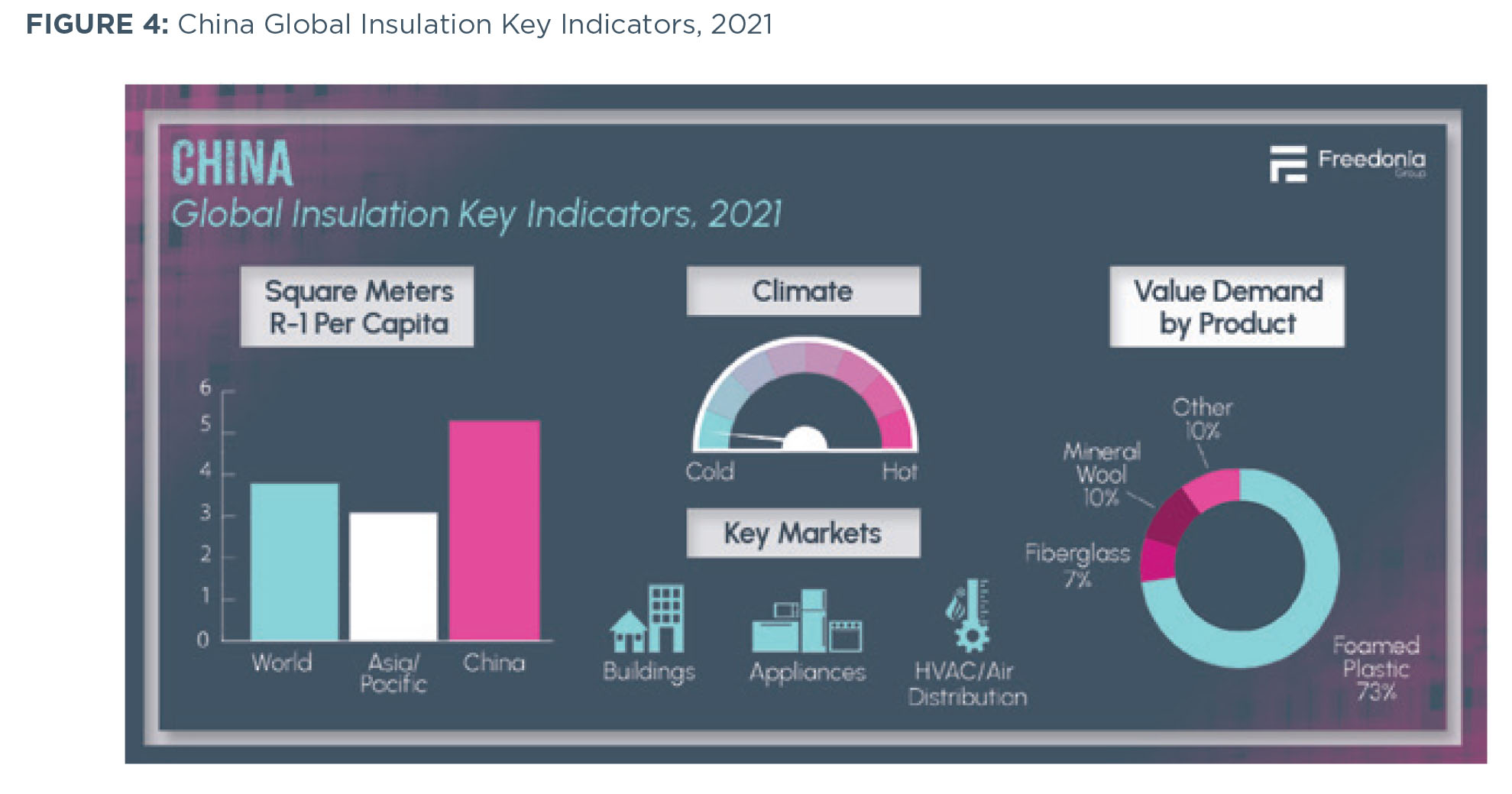

China

Demand for insulation in China totaled $10.4 billion in 2021, accounting for 52% of regional demand. It is the second-largest national market in the world, in value terms, behind the United States. However, China is the largest insulation market when demand is measured in square meters of R-1 value or metric tons (see Figure 4), as the size of the construction

market in China is much larger than that of the United States.

China’s significant insulation market is supported by:

- The largest nonresidential building construction sector in the world;

- A large and expanding housing stock;

- Rising standards of living;

- Government efforts to increase the quality of residential buildings;

- Being the largest appliance manufacturing industry globally; and

- Having large industrial, transportation, and HVAC equipment industries.

China’s massive construction and industrial markets contribute to its high levels of insulation demand. However, intensity of insulation use relative to the population is lower than in more developed countries in the region, including Japan and Australia. China’s generally moderate climate, traditional building practices, and relatively low living standards are responsible for the underutilization of insulation materials. Nevertheless, the Chinese government has imposed updated insulation requirements for residential, public, and energy-efficient green buildings to reduce energy consumption in the country. By 2026, demand for insulation in China is projected to reach $11.4 billion, on annual growth of 1.9%.

Foamed plastic accounted for the vast majority of the insulation demand in China in 2021, supported by the country having the largest appliance and nonresidential building markets in the world. However, fiber glass and mineral wool insulation

are popular in construction applications due in part to superior fire resistance.

- Foamed plastic insulation volume demand will continue to grow at a healthy pace due to its extensive use in the country, especially in appliance manufacturing, such as refrigerator and freezer production.

- However, concern about a series of building fires in China in the past 2 decades has resulted in an increase in the use of mineral wool for the nonresidential building market, due to its fire protection properties.

- Volume demand for other insulation materials is expected to be less strong, as the country continues its shift to more traditional insulation products.

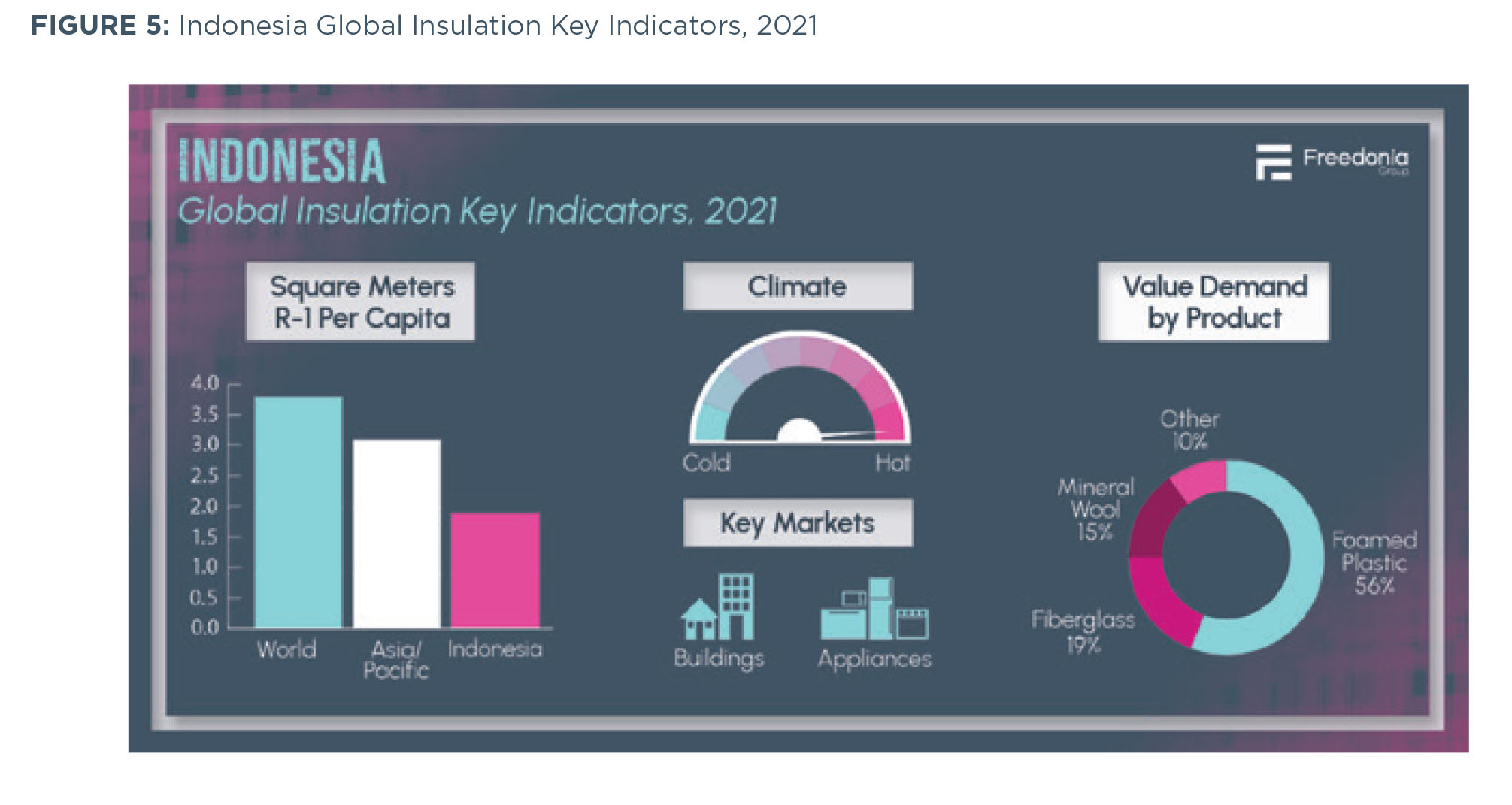

Indonesia

In 2021, demand for insulation in Indonesia was $485 million, representing 2% of regional demand. The size of the country’s insulation market is supported by the world’s fourth-largest housing stock and experiencing significant manufacturing activity. However, the domestic insulation market continues to be restricted because of the generally low quality of the building stock and low standards of living.

Intensity of insulation usage in Indonesia on a per capita basis is below the regional average, as the country possesses a warm climate and low incidence of air conditioning usage. In addition, construction firms primarily employ traditional building techniques and materials that do not include large amounts of insulation.

Through 2026, demand for insulation in Indonesia is projected to grow 3.5% per year, to

$574 million. Increases in demand for foamed plastic, fiber glass, mineral wool, and other materials are all expected to outpace the global average, supported by ongoing expansion of the country’s building stock. (See Figure 5)

Foamed plastic will continue to account for the majority of insulation demand in value terms. Suppliers of these products benefit from the widespread availability of the material in the region and the importance of the nonresidential building and appliance manufacturing sectors to the domestic insulation market. Fiber glass insulation remains popular in residential construction applications.

To Learn More

To find out more about the rest of the Global Insulation demand forecast, visit www.freedoniagroup.com.

Corinne Gangloff is a Marketing Manager for The

Freedonia Group (www.freedoniagroup.com), a division of MarketResearch.com. The Freedonia Group is a leading supplier of industrial and consumer market research, offering content across a broad range of interconnected industries, with a focus on construction, packaging, consumer goods, vehicles and equipment, and chemicals.