How insulation professionals can move from knowing their value to proving it—and persuading others

Mechanical insulation has long been one of the most effective tools for improving building performance. It reduces energy loss, controls moisture, protects equipment, and extends the service life of mechanical systems. Few building components deliver such a strong combination of energy savings, risk mitigation, and durability with such a short payback period.

Within the mechanical insulation industry, these benefits are well understood. They have been reinforced through decades of field experience, engineering guidance, and operational data. Insulation professionals know that when systems are properly insulated, buildings and systems perform better, last longer, and cost less to operate.

What is changing now is not the value of insulation, but the environment in which that value must be communicated.

Design-build delivery is becoming the dominant construction model. Energy codes are evolving into carbon-performance frameworks. Owners, investors, and regulators increasingly expect verification, documentation, and measurable results rather than assumptions. In this environment, insulation is no longer just a supporting system, quietly doing its job in the background. It is becoming central to energy efficiency, emissions reduction, risk management, and long-term asset performance.

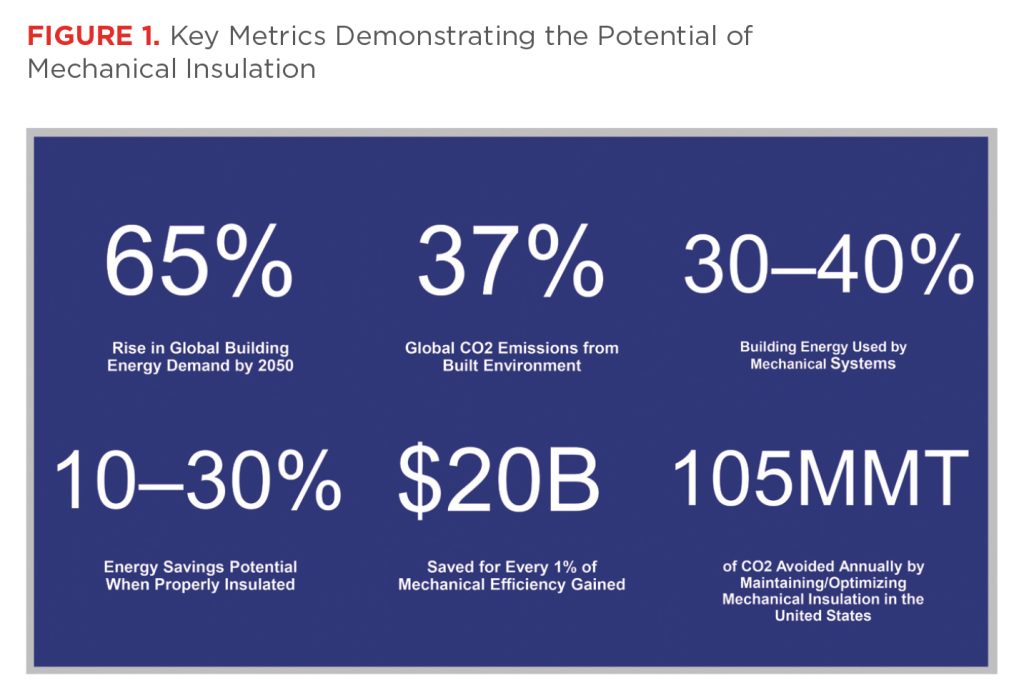

The opportunity facing the mechanical insulation industry today lies in translating the value of insulation clearly and convincingly to the people who define project priorities. This article explores how design-build delivery, decarbonization imperatives, and performance verification are reshaping the role of mechanical insulation—and how insulation professionals can carry that story into broader conversations where decisions are actually made. Figure 1 offers an overview of key trends and statistics at the foundation of the discussion.

The Design-Build Shift: Why Delivery Method Changes Everything

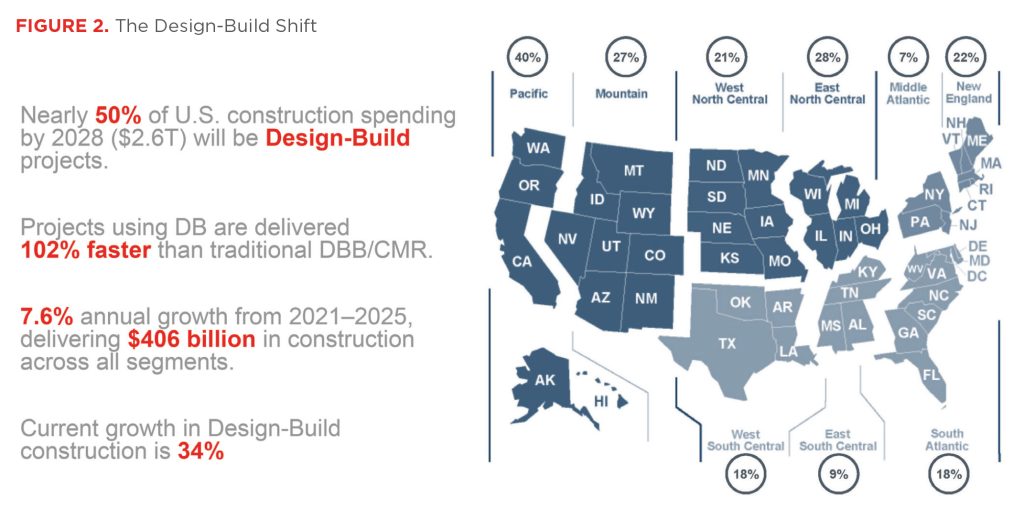

Design-build is no longer an alternative delivery method; it is quickly becoming the default (see Figure 2). By 2028, nearly half of all U.S. construction spending—more than $2.6 trillion—is expected to be delivered through design-build. Projects using this model are completed faster, with fewer change orders and greater alignment between design intent and construction reality.

The reason is simple: Design-build collapses silos.

Instead of design decisions being finalized in isolation and handed downstream for execution, design-build integrates designers, contractors, and specialty trades early. Performance targets such as energy use intensity (EUI), decarbonization goals, cost certainty, and constructability are established collaboratively, at a point where they can still meaningfully influence outcomes.

For mechanical insulation, this shift is foundational.

In traditional design-bid-build projects, insulation decisions often occur late in the process. Specifications may be inherited from previous jobs, copied without climate-specific review, or treated primarily as procurement documents. Insulation becomes something to “fill in” after mechanical systems are designed, rather than a vital system that shapes how those mechanical systems perform.

By the time insulation-related issues such as condensation risk, insufficient thermal continuity, or incompatible materials emerge, the systems are already installed. Corrections at that stage can cost three to five times more than addressing the issue during design, often resulting in rework, delays, and finger-pointing.

Design-build changes that sequence.

When insulation expertise is engaged early, performance criteria are defined before mechanical systems are locked in. Insulation continuity and moisture control strategies can be intentionally designed. Energy models and life-cycle assessments can reflect actual system behavior instead of assumptions. Long-term maintenance, inspection access, and durability considerations can be addressed before they become operational liabilities.

Design-build is not simply a faster way to build. It is a structural opportunity for insulation professionals to move from downstream execution to upstream influence, and to shape performance outcomes instead of reacting to them.

The Specification Reset: Why Many Specs No Longer Match Reality

Despite advances in insulation materials, modeling tools, and codes, many mechanical insulation specifications remain outdated. It is still common to encounter specifications that predate ASHRAE 90.1-2016, rely on minimum R-values without climate zone context, or fail to address condensation risk, moisture migration, and long-term performance degradation.

Such specifications persist not because they are effective, but because they are familiar. Over time, they become institutional defaults, copied from project to project with minimal scrutiny.

The consequences are well known across the mechanical insulation industry:

- Under-insulated systems and unnecessary energy loss;

- Moisture intrusion, mold growth, and corrosion under insulation;

- Disputes over responsibility when systems fail to perform as expected; and

- Increased maintenance costs and premature equipment failure.

Ambiguous specifications frequently reinforce a lowest-bid mentality rather than performance-based decision-making. In that type of environment, insulation becomes a cost to minimize instead of a solution to optimize.

Design-build delivery offers an opportunity to reset this pattern.

Modern, performance-based specifications can reference current standards such as ASHRAE 90.1-2022, and ASHRAE 90.4 for data centers, updated ASTM testing methods, and IECC 2024 requirements. More importantly, they can articulate expected outcomes rather than just prescriptive minimums. Thermal continuity, operating temperature ranges, vapor barrier integrity, and maintenance considerations can be explicitly addressed.

This shift reframes insulation from a static section of the specification book into a living performance strategy aligned with energy, carbon, and durability goals.

The Hidden Return on Investment of Mechanical Insulation

Mechanical insulation consistently delivers one of the strongest returns on investment in the built environment, yet its value is often under-communicated to decision-makers.

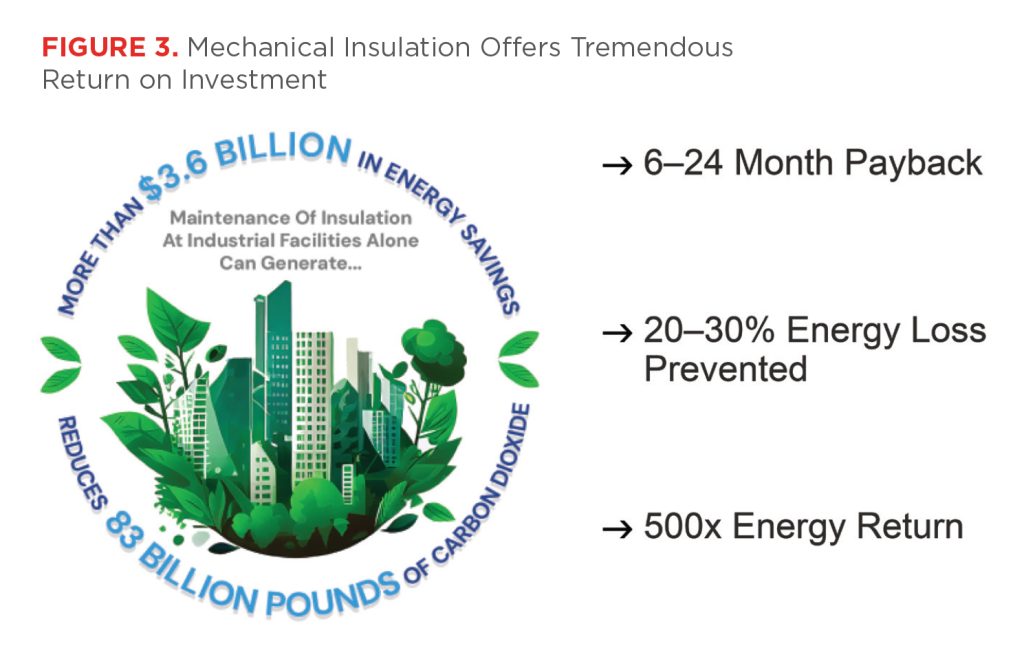

Typical insulation improvements deliver payback periods of 6 to 24 months. Properly insulated mechanical systems can prevent 20 to 30% of energy loss, particularly in heating and cooling systems where temperature differentials are high. Over the life of a building, cumulative energy savings often exceed the energy required to manufacture and install insulation by orders of magnitude (see Figure 3).

Unlike many efficiency upgrades, insulation performance compounds. Once installed correctly, it continues delivering savings every hour the system operates.

Beyond energy savings, insulation provides additional benefits that resonate strongly with owners and operators when articulated clearly:

- Reduced maintenance and repair costs,

- Protection of high-value mechanical equipment,

- Improved system reliability and uptime,

- Enhanced personnel safety,

- Lower risk of moisture-related failures, and

- Extended asset life and deferred capital replacement.

When insulation is framed only as a code requirement or a commodity line item, all the benefits listed above are rarely captured in decision-making. When it is framed as an operational and financial asset—one that reduces risk while improving performance—insulation becomes much harder to skim on and much easier to defend during value engineering.

From Energy Efficiency to Carbon Accountability

The conversation around building performance is expanding beyond energy efficiency to include carbon accountability.

Recent code updates reflect this shift. ASHRAE 90.1-2022 and ASHRAE 90.4 emphasize thermal continuity and verified R-values rather than assumed performance. IECC 2024 further strengthens requirements related to insulation design and installation quality. At the same time, federal mandates, climate disclosure rules, and corporate Environmental, Social, and Governance (ESG) commitments are increasing pressure on owners to account for Scope 1 and Scope 2 emissions.

Mechanical insulation directly affects both.

By reducing energy demand, insulation lowers the emissions associated with on-site fuel combustion and purchased electricity. It also supports system longevity, reducing the frequency of equipment replacement and the associated embodied carbon impact over time.

Yet despite this influence, insulation performance is still often assumed rather than verified. Projects are closed out with modeled energy savings that may never be validated in operation. When that happens, gaps emerge between design intent and reality, representing uncounted emissions, lost savings, and missed opportunities for improvement.

Verification closes that loop.

Thermal imaging, surface temperature measurements, digital documentation, and integration with Building Information Modeling (BIM) or digital twin platforms allow teams to confirm that insulation performs as intended. Verification protects return on investment, ensures performance persistence, and provides data that owners can use for regulatory compliance, sustainability reporting, and capital planning.

In this context, insulation is no longer just a thermal control measure—it is a carbon management strategy.

Design Variables that Drive Long-Term Performance

Several key variables determine whether insulation delivers its intended benefits over time.

Temperature differential (ΔT) defines the magnitude of heat loss or gain across mechanical systems. The greater the differential, the greater the energy and carbon impact of inadequate insulation. Thermal conductivity (λ) determines how effectively a material resists heat flow and directly affects system efficiency.

Continuity is equally critical. Gaps, compression, penetration, and thermal bridges undermine performance and increase energy demand. Moisture barrier integrity protects insulation performance over time; once compromised, R-values degrade rapidly, eroding both energy and carbon benefits. Finally, maintenance factors ensure persistence. Even well-designed systems lose performance without inspection, repair, and upkeep.

Design-build delivery allows these variables to be addressed holistically rather than piecemeal, improving long-term outcomes and reducing operational risk.

Data Centers and Emerging Trends: Where the Future Is Already Visible

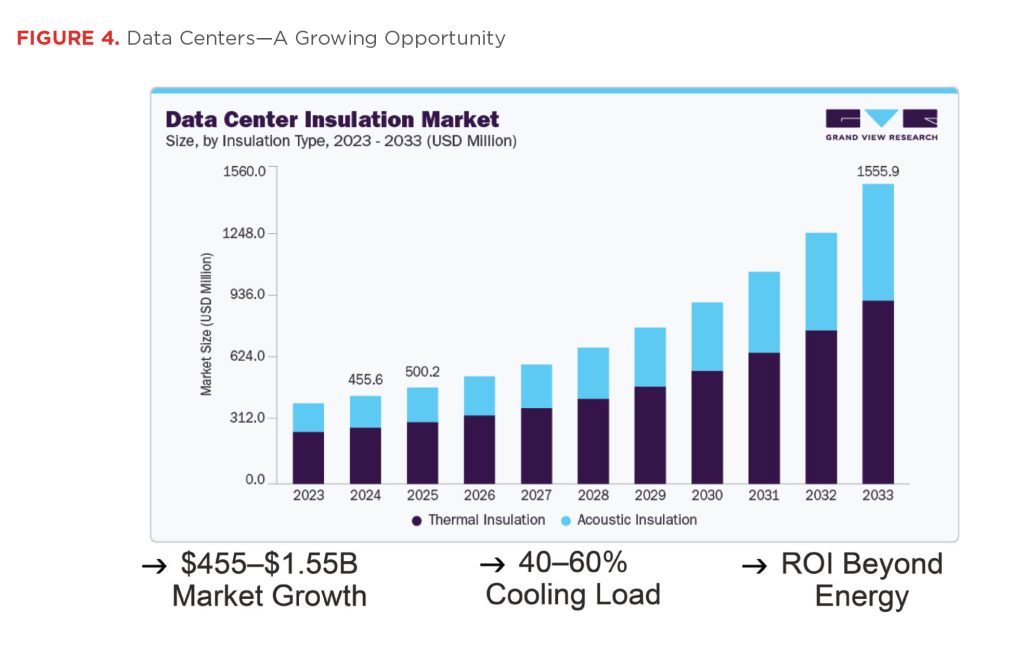

Data centers offer a clear view of where insulation practice is headed (see Figure 4).

Globally, data centers consume approximately 3 to 4% of total electricity, and that share continues to rise with the expansion of cloud computing, artificial intelligence, and digital infrastructure. Hyperscale facilities can contain tens of thousands of linear feet of insulated piping and ductwork, some exceeding 30 inches in diameter.

In these environments, insulation performance is mission critical.

Condensation control, thermal precision, and reliability directly affect uptime. A single insulation failure can cascade into equipment damage, operational disruption, and significant financial loss. As a result, data center owners demand higher levels of documentation, quality assurance, and verification than owners of other building types.

These projects also highlight broader trends in reshaping the insulation industry:

- Early insulation design for prefabricated and modular mechanical systems;

- Insulation as a schedule-critical component rather than a finishing trade;

- Integration of insulation data into BIM and digital monitoring platforms; and

- Owner expectations for measurable, documented performance.

What begins with mission-critical facilities rarely stays there. Similar expectations are now emerging in health care, advanced manufacturing, and large campus projects, signaling a broader shift toward visible and verifiable insulation performance.

Moving the Conversation Upstream: How Insulation Professionals Can Convince Everyone Else

For many professionals reading this article, none of this information is new. The challenge is not understanding insulation’s value. Rather, it is communicating that value to people who do not live in mechanical rooms.

Owners, developers, finance teams, and even some design professionals are not dismissive of insulation, but they are focused on different metrics. They speak in the language of risk, return, compliance, and accountability. To move insulation upstream in decision-making, insulation professionals must meet those audiences where they are.

That begins by shifting the conversation from what insulation is to what insulation does.

Leading with R-values, thicknesses, or material types rarely resonates outside the industry. Leading with outcomes does. Cost savings, emissions reduction, operational resilience, and risk mitigation are universally understood.

Project workflows already provide natural opportunities to communicate insulation’s value. Early design meetings, value engineering discussions, sustainability briefings, capital planning reviews, and commissioning closeouts all create moments where insulation can be positioned as a performance lever instead of a cost.

Tying insulation decisions to what others are accountable for is equally powerful. Energy budgets, ESG disclosures, equipment uptime, maintenance costs, and regulatory compliance all intersect with insulation performance. Making that connection explicit changes how insulation is perceived.

Visibility matters as well. When insulation performance is verified and documented, it becomes tangible. Thermal images, surface temperature data, and performance reports turn insulation from an assumption into proof—and proof travels far beyond the mechanical room.

Perhaps most importantly, insulation professionals must embrace a broader role. When they show up as downstream installers, they are treated that way. When they show up as performance partners, armed with data, life-cycle thinking, and cross-disciplinary awareness, the conversation changes.

This is not about louder advocacy. It is about smarter translation.

The Road Ahead: From Hidden to Essential

Mechanical insulation is entering a new era: one defined by integration, verification, and visibility.

Digital tools are making insulation performance traceable. Codes and standards are embedding carbon accountability. Owners are demanding proof, not assumptions. These shifts favor solutions that are proven, durable, and cost-effective. Insulation meets all three of these points—when it is designed, installed, and communicated intentionally.

The future of mechanical insulation is not about convincing the industry of its own importance. It is about carrying that importance into conversations where priorities are set and budgets are allocated. When insulation professionals speak in the language of performance, risk, and carbon reduction, insulation moves from being quietly important to undeniably essential.